A lot of near-retirees are sitting with the same uneasy habit right now. They open a 401(k) statement, see the balance, and then wonder how much of that buying power will still feel real after more inflation, more market swings, and another decade of withdrawals.

That's where a Gold IRA enters the conversation. Not as a magic fix, and not as a replacement for everything else, but as a diversification tool that deserves a hard, skeptical comparison before any rollover happens.

Is a Gold IRA the Right Move for Your Retirement Savings

You are a few years from retirement. Your account balance looks solid on paper, but one bad market stretch right before withdrawals could change the math fast. That is usually the moment people start asking whether part of their savings should sit in something they can understand more plainly and worry about less.

A Gold IRA can serve that purpose for the right person. It gives a retirement portfolio some exposure to physical metal inside a tax-advantaged account. What matters is using it with discipline.

My view is simple. A Gold IRA works best as a limited diversification position, not a full retirement strategy. If you are considering one, focus less on the sales pitch about gold itself and more on what ownership will cost you over time and how easily you can sell after the rollover is done. Total lifetime cost of ownership and post-rollover liquidity usually have more impact on retirement results than the headline setup fee.

When a Gold IRA usually makes sense

A Gold IRA is often a reasonable fit if you want:

- A hedge against concentration in paper assets: Many near-retirees already have heavy exposure to stock and bond funds through workplace plans

- A long time horizon: Physical metals are generally better suited to patient holders than to short-term traders

- A measured allocation: Gold should usually be one part of the plan, not the plan itself

- Clear eyes about trade-offs: You are willing to accept storage fees, custodian fees, and slower selling in exchange for diversification

That last point gets missed all the time. Two companies can look similar on annual fees and still leave you with very different long-term outcomes if one adds high markups on the metal or makes liquidation expensive and slow later.

When it probably does not

A Gold IRA is usually a poor fit if your top priority is:

- Fast access to cash

- Low ongoing account costs

- A small rollover amount that fees could eat into

- A simple set-it-and-forget-it account with minimal paperwork

- Maximum income production, since physical gold does not pay interest or dividends

Gold can reduce one kind of anxiety while creating another. Many investors feel better owning a hard asset, then get frustrated when they learn the actual friction shows up after purchase, especially if they need to sell quickly or discover the dealer's buyback terms are weak.

Bottom line: A Gold IRA makes sense for investors who want a modest allocation to physical metals and who fully understand the lifetime costs, storage rules, and exit options before they transfer a dollar.

The right decision comes from comparing the full ownership experience. Not just annual fees, but dealer spreads, storage charges, custodial costs, and the quality of the buyback policy you may need later in retirement.

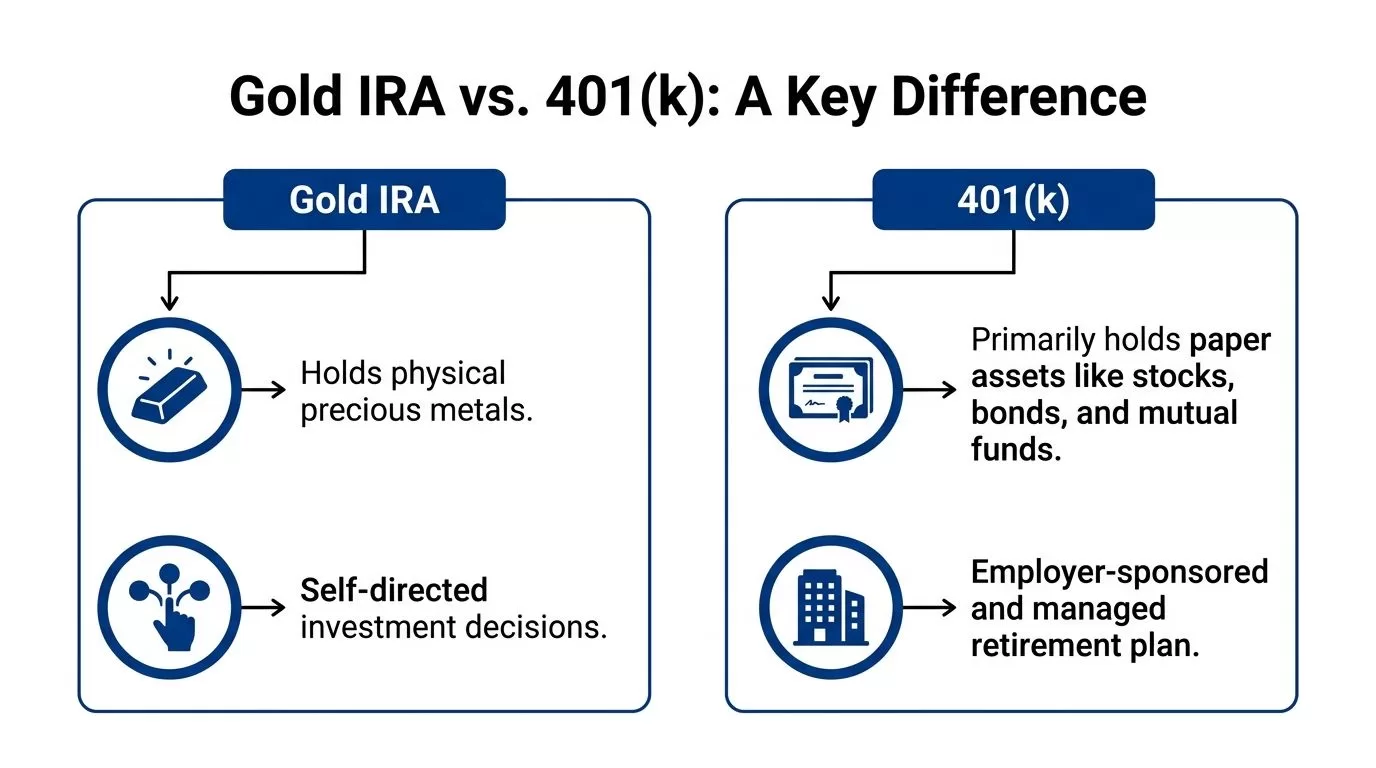

How a Gold IRA Works Differently Than Your 401k

You may log into a 401(k), click a fund, and be done in under a minute. A Gold IRA does not work that way. It uses the same retirement-account tax framework, but the actual ownership process is slower, more regulated, and more expensive to maintain over time.

A 401(k) is built around paper assets held inside a workplace plan. A Gold IRA is a self-directed IRA that holds IRS-approved physical bullion through a custodian and approved storage facility. That difference changes the paperwork, the trading experience, the fee structure, and your options when you want cash later.

A Gold IRA has more parties involved

With a standard 401(k), the plan administrator and investment platform handle most of the heavy lifting behind the scenes. A Gold IRA splits those responsibilities across several players:

- The account owner: Directs the account and approves transactions

- The custodian: Handles IRA administration, reporting, and compliance

- The metals dealer: Sells the coins or bars that meet IRA rules

- The depository: Stores the metal in an approved vault

That structure is not a minor detail. It is the reason Gold IRAs usually involve more forms, more coordination, and more points where costs can be added.

The tax rules are familiar. The asset rules are not.

A Gold IRA can be set up as a Traditional IRA or a Roth IRA. The tax treatment follows the normal IRA rules. Traditional accounts are generally funded with pre-tax dollars and taxed at withdrawal. Roth accounts are funded with after-tax dollars, and qualified withdrawals are tax-free.

The unusual part is not the tax wrapper. The unusual part is what the account is allowed to hold, how that metal must be purchased, and where it must be stored.

The IRS does not let you buy just any coin, put it in a home safe, and call it IRA property. The metal has to meet eligibility rules, and it has to stay under approved custody. If you want a clearer picture of the ongoing charges tied to that setup, review this breakdown of how much Gold IRA fees can cost.

Liquidity is slower, and that matters more than many investors expect

Many near-retirees are often surprised by this.

In a 401(k), selling a mutual fund is usually simple. In a Gold IRA, liquidation often means contacting the custodian, getting the sale approved, coordinating with the dealer or buyback desk, and waiting for settlement. That process can feel manageable when markets are calm. It feels very different when you need cash on a deadline.

This is one of the biggest reasons a smart gold IRA comparison should go beyond annual custodial fees. Long-term cost is not just what you pay to hold the account. It is also what you give up in flexibility, pricing spread, and speed when you sell.

The biggest cost difference often shows up after the rollover

A 401(k) investor usually focuses on expense ratios and plan fees. A Gold IRA investor also has to account for dealer markups, storage charges, custodial fees, and the gap between the price paid for metal and the price offered later in a buyback.

That last point deserves more attention than it gets. Two Gold IRAs can look similar at setup and still produce very different outcomes over a decade or more if one provider charges aggressive markups upfront or offers weak repurchase terms later.

A 401(k) is designed for convenience and fast trading. A Gold IRA is designed for holding a specialized physical asset under retirement-account rules.

If you understand that trade-off before you roll money over, you are far less likely to make an expensive mistake.

The 7 Critical Criteria for Your Gold IRA Comparison

A weak gold IRA comparison focuses on whatever makes the first phone call sound cheap. A useful one shows what the account is likely to cost you over many years, and how hard it may be to turn those metals back into cash when retirement spending starts.

That is the standard to use here.

1. Total lifetime cost matters more than the headline fee

The annual admin fee is only one line item. Your real cost also includes setup charges, storage, dealer markup on the metal you buy, and the spread you face when you sell later.

That is why smart investors ask for a full written fee schedule before any rollover paperwork begins. If you want a clear breakdown of the cost categories to review, start with this guide on how much Gold IRA fees can cost.

2. Custodian quality affects compliance and day-to-day execution

A Gold IRA is not just a metal purchase inside a retirement wrapper. It depends on a qualified custodian, accurate paperwork, and clean coordination between the custodian, dealer, and depository.

Sloppy administration creates risk you do not need. Delays, unclear records, and preventable errors usually show up later, right when you need a distribution, sale, or required minimum distribution handled correctly.

3. Metal eligibility rules must be checked before you buy

This is a common place for expensive mistakes. IRA-approved metals have to meet IRS standards for purity and product type. Gold generally must meet a 99.5% fineness standard, with a limited exception for the American Gold Eagle.

The practical takeaway is simple. Do not buy based on a sales pitch, a collectible story, or a flashy coin presentation. Confirm in writing that every product offered for the IRA is eligible.

4. Storage details should be clear, specific, and in writing

“Stored in an approved depository” is not enough information. You should know where the metals are held, whether your holdings are segregated or non-segregated, what insurance applies, and what each option costs.

Ask these questions directly:

- Which depository will hold the metals?

- Is storage segregated or commingled?

- What does each storage option cost each year?

- What insurance protection applies while the metals are in storage?

- What is the process for verifying holdings if questions come up later?

5. Buyback policy has a bigger retirement impact than sales materials suggest

This point gets overlooked, and it should not. Post-rollover liquidity matters.

A provider's buyback process affects how quickly you can raise cash, what pricing method is used, who approves the sale, and how much of a spread stands between you and your money. Two accounts with similar annual fees can produce very different results if one firm offers poor repurchase terms or a slow liquidation process.

Ask for clear answers on these points before you fund the account:

- How is the sell-back price determined?

- Is there a standing buyback program or only case-by-case offers?

- How long does liquidation usually take from request to settlement?

- Are there extra transaction charges when you sell?

- Can partial liquidations be handled easily?

If a company cannot explain its buyback process in plain English, do not trust it with retirement assets.

6. Service quality matters because the process has moving parts

A Gold IRA involves transfer forms, account setup, metal selection, custodian coordination, depository logistics, and later distribution questions. You need a team that answers directly and follows through.

Good service looks boring, and that is a compliment. Calls get returned. Documents arrive on time. Questions get straight answers. Retirement money should not depend on a salesperson who disappears after the rollover clears.

7. Education should reduce mistakes, not support a sales script

Good education helps you judge trade-offs clearly. Weak education keeps the focus on fear, urgency, and promotional offers.

Look for firms that explain fee structure, product eligibility, storage choices, distribution rules, and liquidation steps without rushing you. If the conversation stays centered on “free” silver or limited-time incentives, you are not getting advice. You are getting a pitch.

Side-by-Side Analysis of Top Gold IRA Companies

A near-retiree rolls over a large 401k balance into gold, feels relieved, then learns two years later that selling part of the account is slower, more expensive, and less predictable than expected. That is the mistake a good comparison should prevent.

Many Gold IRA reviews still focus on flashy rankings, low-looking first-year fees, or polished sales language. That misses the two issues that matter most over a long retirement: total lifetime cost of ownership and post-rollover liquidity.

Use this section to compare provider types, not marketing claims. If you want a broader shortlist before applying this filter, review these top Gold IRA companies and then judge them by long-term cost and ease of exit.

Gold IRA Provider Comparison at a Glance 2026

| Provider Type | Minimum Investment | Cost Pattern | Storage | Liquidity and Buyback Pattern |

|---|---|---|---|---|

| Education-first provider | Varies by firm | Often presents fees more clearly upfront, but still needs a full written breakdown of setup, custody, storage, insurance, and metal pricing | IRS-approved depository structure | Usually better at explaining the process, but written sell-back terms still matter more than verbal reassurance |

| Low-minimum provider | Varies by firm | Can look accessible early, but smaller accounts can feel annual fees more heavily as a percentage of assets | IRS-approved depository structure | Investors should confirm whether partial liquidations are handled efficiently |

| Promotion-heavy provider | Varies by firm | Intro offers can distract from spreads, product markups, and long-term holding costs | IRS-approved depository structure | Buyback language is often less prominent than the sales pitch. That is a warning sign |

| Service-first provider | Varies by firm | May charge more, or may simply explain pricing better. You need the all-in cost in writing either way | IRS-approved depository structure | Often a better fit for anxious retirees if liquidation steps, timing, and pricing method are documented clearly |

Total lifetime cost of ownership is the real test

Annual admin fees matter. They are only one piece of the bill.

The bigger drain usually comes from the full chain of costs over time: account setup, custodial fees, storage, insurance, dealer spread, product markup, and the pricing gap when you eventually sell. A provider can look reasonable in year one and still cost far more over a 15 to 25 year holding period than you expected.

That is why I do not recommend choosing a Gold IRA company based on the lowest advertised annual fee alone.

A better question is this: what will this account cost me from rollover to final liquidation?

Ask each firm for a written estimate that covers:

- one-time setup charges

- annual custody and storage fees

- whether fees are flat or asset-based

- typical markup range on the metals you are considering

- expected spread between buy and sell pricing

- any fees tied to liquidation, shipping, or account closure

If a company will not put those details in writing, move on.

Post-rollover liquidity matters more than the sales process

Opening the account is usually organized and pleasant. The true quality test comes later, when you want cash out of the account.

Retirees do not sell because they made a mistake. They sell because life happens. Required distributions begin. Medical costs show up. A portfolio rebalance makes sense. You want a provider that treats liquidation as a standard service, not as an inconvenience.

Strong firms make the exit process clear before you fund the account. Weak firms stay vague until your money is already in place.

Look for direct answers on:

- how a sale request is submitted

- whether the company has a standing buyback program

- how the sale price is calculated

- how partial sales are handled

- how long settlement usually takes

- whether any extra transaction charges apply when you sell

A company with polished onboarding and fuzzy liquidation terms is not a strong choice for retirement money.

Which provider type usually fits best

The best fit depends less on branding and more on your priorities.

If you want hand-holding, choose a provider that answers plainly, documents everything, and does not rush you into specific coins. If you care most about keeping costs down, press hard on spreads, markups, and long-term storage costs. If access to cash later is your top concern, put buyback rules ahead of promotions, freebies, and sales bonuses.

My recommendation for most cautious near-retirees is simple. Favor the firm that gives you clear written answers on lifetime cost and liquidation before any rollover starts.

That provider is usually the safer choice.

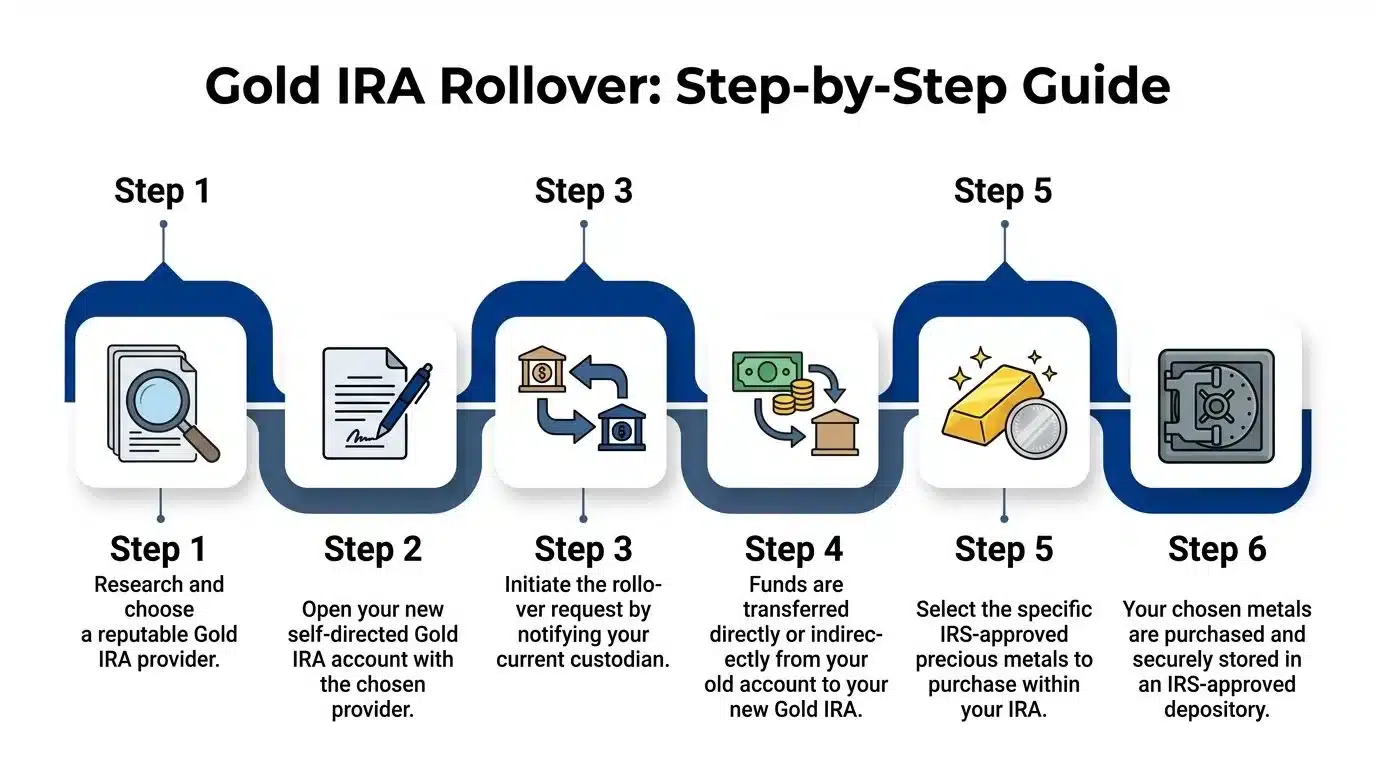

How to Complete a Gold IRA Rollover Step by Step

A rollover usually feels stressful for one reason. You are moving retirement money through a process you do not do often, while salespeople may be pushing you to hurry.

Do not hurry.

The safest rollover is boring, papered, and easy to explain after the fact. Your job is to keep control of the sequence so costs, eligibility, and liquidation terms are clear before money leaves your current account.

Step 1 Choose the provider and custodian first

Pick the firm before you touch the old account. That sounds obvious, but many retirees start the paperwork before they have pinned down the full fee schedule, storage setup, metal markups, and sale process.

Your comparison work pays off. Focus on total lifetime cost of ownership, not just the annual admin fee. A provider with a lower yearly charge can still cost more over time if its metal spread is wide or its buyback terms are weak. Ask for written answers before you sign anything.

Step 2 Open the self-directed IRA

The new custodian opens the account and gives you the forms needed for the transfer or rollover. Until that account exists, the money has nowhere to go.

Read the account documents closely. Confirm the account title, beneficiary details, fee disclosures, and storage arrangement now, while changes are still easy.

A visual walkthrough can help make the process less abstract:

Step 3 Request a direct transfer or rollover

For many investors, a direct trustee-to-trustee transfer is the cleanest option when it is available. The money moves between institutions instead of passing through your bank account.

That lowers the chance of avoidable tax trouble and missed deadlines. If a representative keeps steering you toward a method that puts the funds in your hands first, slow down and ask why.

Step 4 Choose IRS-approved metals carefully

After the cash reaches the new IRA, you select the metals for purchase. Keep this part simple. Stick to IRA-eligible bullion and get the exact product, quantity, and pricing confirmed in writing before the trade is placed.

This is also the moment to pay attention to liquidity. Some products are easier to resell than others, and that matters later if you need partial distributions or want to raise cash. A rollover is not complete planning if you only focus on how to buy and ignore how you may need to sell.

Step 5 Confirm approved depository storage

IRA metals must be stored through a qualified custodian and approved depository to keep the account in compliance. Home storage is not a valid shortcut for IRA assets.

Get the storage details in writing. You want to know where the metals are held, whether the storage is segregated or non-segregated, how insurance is handled, and what records you will receive after the purchase settles.

Step 6 Save every document and review the account each year

Keep your account agreement, transfer forms, trade confirmations, storage records, and annual statements together. If there is ever a pricing dispute, distribution question, or beneficiary issue, your paperwork matters.

Review the account once a year with fresh eyes. Check whether the fees still make sense, whether the holdings still fit your plan, and whether the company's liquidation process still looks workable for the retirement years ahead.

A good Gold IRA rollover should feel controlled, documented, and a little dull. That is usually a sign you handled it the right way.

Common Pitfalls and High-Pressure Tactics to Avoid

A lot of near-retirees make the same mistake. They spend hours comparing annual fees, then get pushed into a rollover without asking what it will cost to sell later or how hard it will be to get cash out when retirement needs change.

That is how expensive surprises happen.

The biggest investor mistakes

The first mistake is comparing Gold IRAs by annual fees alone. Setup charges, storage costs, custodian fees, dealer markups, shipping, and the spread between buy and sell prices all affect your real outcome. The number that matters is total lifetime cost of ownership, especially if you may hold the account for years and eventually need partial liquidations.

The second mistake is ignoring post-rollover liquidity. Some metals are easier to resell than others, and some firms make their buyback process sound better than it is. If the company will not explain its repurchase terms, timing, pricing method, and any transaction costs in plain writing, move on.

A third mistake is assuming every gold product qualifies for an IRA. It does not. Eligibility rules are specific, and mistakes can create tax trouble. Review the precious metal IRA rules before any purchase is placed, not after the account is funded.

Paperwork matters here. So does patience.

The sales tactics that deserve skepticism

High-pressure firms usually rely on emotion, not clarity. Watch for these warning signs:

- Urgency scripts: claims that you need to act today or miss a narrow window

- Home storage pitches: suggestions that you can keep IRA metals at home and stay compliant

- Guaranteed claims: promises of safety, protection, or returns

- “Free” silver or bonus metal offers: promotions that often get paid for through higher pricing

- Vague buyback language: no written explanation of how liquidation works or what price standard is used

- Resistance to outside review: discomfort when you ask to speak with your advisor, CPA, or attorney before signing

One red flag should slow you down. Several should end the conversation.

A trustworthy Gold IRA firm should be willing to answer hard questions about fees, spreads, storage, and liquidation in writing. If the conversation turns slippery when you ask what selling will look like later, that is your answer.

Retirement money should go only into an account you understand from purchase through eventual sale. If the firm cannot explain the full cost to own it and the full process to exit it, do not hand over your rollover.

Frequently Asked Questions About Gold IRAs

What is the usual minimum investment for a Gold IRA

Minimums vary a lot by firm. Some accept a modest rollover. Others expect a much larger opening balance.

Do not treat this as a small detail. A higher minimum can push you into funding more than you intended, and that matters if you are still deciding how much of your retirement savings belongs in metals in the first place. Ask for the minimum in writing, along with the full fee schedule, the dealer spread, and the company's buyback terms. That gives you a clearer picture of total lifetime cost, not just the cost to open the account.

For account eligibility, approved metals, and storage standards, review these precious metal IRA rules before you fund anything.

Can someone contribute to a Gold IRA every year

Yes, if they qualify to make IRA contributions under normal IRS rules.

The key point is simple. A Gold IRA does not get a special contribution cap just because it holds metals. It follows the same annual contribution framework as other IRAs. If you are rolling over old retirement money, that is a separate process from making a new annual contribution, and people often confuse the two.

When do required minimum distributions start

Traditional Gold IRAs are subject to required minimum distributions.

That matters more with physical metals than with paper assets. You cannot sell a fractional corner of a gold bar the way you can sell a slice of a mutual fund. If your account is built with larger coins or bars, liquidation can be clumsy at the exact time you need precision. This is one reason I put post-rollover liquidity near the top of any Gold IRA comparison. A company with vague repurchase policies can create real headaches later.

Can metals from a Gold IRA be stored at home

No.

IRA-owned metals must be held through an approved custodian and stored in a qualified depository. If a salesperson suggests home storage while calling it IRA-compliant, walk away. That pitch is a tax problem waiting to happen.

Is a Gold IRA better than owning gold directly

It depends on what you want the gold to do.

A Gold IRA puts the metal inside a retirement account structure, which can make sense for rollover dollars you want to keep in that tax-advantaged framework. Direct ownership gives you personal possession and simpler access, but it does not operate under IRA tax rules.

For near-retirees, the better question is often not “Which is better?” It is “Which is easier to live with later?” If you may need to raise cash quickly, review the exit process before you buy. The annual fee gets attention. The spread you pay to buy, the price standard used when you sell, and the speed of the buyback process often have a bigger effect on what you keep.

This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.

If a rollover is on the table, compare companies with a written checklist built around lifetime ownership cost, storage terms, and liquidation policies. Gold IRA Association offers educational guides, provider comparisons, and a low-pressure way to compare top Gold IRA companies or talk through options at 888-910-8386.