Retirement investors often get to the same point. They've decided a Gold IRA may fit their diversification goals, then they hit a confusing term that seems far more technical than expected: custodian.

That confusion matters, because an IRA custodian for gold isn't just paperwork. It's the party that helps keep the account compliant, coordinates storage, and protects the account from mistakes that can trigger taxes and penalties. For anyone nearing retirement, that role deserves careful attention.

Introduction

A common situation looks like this. Someone has an old 401(k) or a traditional IRA, likes the idea of holding some retirement savings in physical gold, and starts researching how to open the account. Then the process suddenly shifts from gold bars and coins to custodians, depositories, forms, and IRS rules.

That's where many readers pause.

A Gold IRA can feel simple in theory and bureaucratic in practice. The missing piece is understanding that the custodian is not a side detail. The custodian is the long-term partner that helps keep the account legal, organized, and secure.

For pre-retirees, this is the proper frame to use. The question isn't only who stores the gold. The better question is who helps protect the entire retirement account from avoidable IRS problems.

Practical rule: In a Gold IRA, the custodian protects more than metal. The custodian helps protect the account's tax-advantaged status.

A good custodian helps with the account setup, handles reporting, works with the depository, and screens purchases so the account stays within IRS rules. A weak custodian, or a poorly understood one, can leave an investor exposed to hidden fees, storage confusion, or prohibited transactions.

What Is a Gold IRA Custodian and Why Is It Required

A Gold IRA custodian is the financial institution that administers a self-directed IRA holding precious metals. It is not the same as the dealer that sells the metals. That distinction causes a lot of confusion.

The dealer helps with the product selection and transaction side. The custodian handles the IRA itself. That means account administration, required reporting, coordination with the storage facility, and oversight of whether the account follows IRS rules.

The custodian's role in plain English

An IRA custodian for gold usually handles tasks like these:

- Opening and maintaining the account so the IRA is properly established and documented

- Processing purchases and sales inside the IRA

- Coordinating with an approved depository where the metals are stored

- Maintaining records and reporting required to preserve the account's tax treatment

- Screening for compliance issues that could turn a retirement asset into a taxable problem

The IRS doesn't treat precious metals in an IRA as many investors might expect.

According to this explanation of IRC Section 408(m) and Gold IRA custody rules, physical precious metals held within an IRA must be managed by an approved custodian and stored in an IRS-approved depository. Personal home storage is prohibited and legally counts as a distribution, which can trigger income taxes and a potential 10% penalty if the account holder is under age 59½.

Why “self-directed” doesn't mean self-stored

The phrase self-directed IRA can mislead people. It sounds as if the investor can buy approved gold and hold it personally. That's not how the rules work.

Self-directed means the investor chooses the asset class. It doesn't remove the legal requirement for qualified custody and approved storage. The account owner directs the investment. The custodian handles the technical side that keeps the IRA compliant.

A Gold IRA is self-directed in investment choice, not self-managed in custody.

What happens if someone tries to bypass the custodian

Here is the practical risk. An investor hears about “home storage” or assumes a personal safe is acceptable. That decision can convert part or all of the account into a taxable distribution.

A simple comparison makes the point clearer:

| Situation | IRS treatment in general terms |

|---|---|

| Gold bought inside the IRA and held through approved custody and depository arrangements | Account remains within IRA structure |

| Gold taken into personal possession or stored at home | Treated as a distribution, with taxes and possible penalty |

That's why the custodian is the single most important operational partner in the account. The custodian isn't there to sell a story. The custodian is there to keep the IRA from breaking the rules.

Eligible Metals and IRS Purity Rules Custodians Enforce

One of the custodian's most important jobs is screening what can and can't go into the account. Many investors assume that any gold coin or bar qualifies. That's not true.

The IRS places fineness requirements on metals held in a precious metals IRA. If the item fails the standard, the purchase can become a prohibited transaction. In practical terms, that means a mistake at the buying stage can create a tax problem before the metal ever reaches storage.

The gold rule most people need to know

According to this Gold IRA custodian due diligence checklist, a gold IRA custodian must enforce a strict 99.5% fineness requirement for gold bullion, with the American Gold Eagle as the sole statutory exception at 91.67% fineness under IRC Section 408(m)(3)(A). If the metal doesn't meet that rule, the IRS can treat the acquisition as a taxable distribution, with ordinary income tax and a potential 10% early withdrawal penalty for investors under age 59½.

That exception surprises many readers. The American Gold Eagle is allowed even though it doesn't meet the standard bullion purity threshold that applies to most other gold products.

Why custodians screen metals so carefully

This is more than administrative nitpicking. The IRS generally treats non-qualifying precious metals as collectibles, and collectibles don't receive the same treatment inside an IRA as approved bullion.

That's why a careful custodian reviews product eligibility before the asset is accepted into the account. The goal is to stop the investor from accidentally buying a beautiful product that doesn't belong in a retirement account.

For a broader overview of product rules, this guide to precious metal IRA rules can help clarify what belongs in an account and what doesn't.

A practical example

Suppose an investor likes the look of a specialty coin marketed as rare or commemorative. It may still be unsuitable for IRA use, even if it contains gold. A strong custodian won't just process the order because the investor asked for it. The custodian acts as a checkpoint.

The safest custodian is often the one willing to say no to an ineligible purchase.

That can feel restrictive in the moment, but it's one of the core protections the custodian provides.

Decoding Custodian Fees and Services

Fees deserve direct attention because they shape the actual cost of holding physical metals in a retirement account. Many investors start with the gold price and stop there. The better approach is to separate the metal cost from the account cost.

The custodian and the depository create an ongoing administrative structure, and that structure isn't free.

The main fee categories

Most Gold IRA costs fall into a handful of buckets:

- Setup fee. A one-time charge for opening the account.

- Annual administration fee. Paid for recordkeeping, reporting, account maintenance, and ongoing custodial support.

- Storage fee. Paid for the secure storage of the physical metals through the approved depository arrangement.

- Purchase premium. This is tied to the metal transaction itself rather than custody alone, but it affects first-year cost in a major way.

According to this analysis of Gold IRA fees and costs, the average annual cost of maintaining a Gold IRA is approximately $250, with custodial and administration fees typically ranging from $75 to $300 per year. The same analysis notes that for a standard $100,000 Gold IRA, first-year expenses can reach about 5.35% of the initial value, and that many investors reduce the impact of fixed fees by starting with $25,000 to $50,000 rather than a smaller account.

What those fees are paying for

A lot of readers ask whether these charges are just overhead. Some are, but several cover real compliance work.

A custodian generally handles:

| Service | Why it matters |

|---|---|

| Account administration | Keeps the IRA active and properly maintained |

| Transaction processing | Ensures purchases and sales are executed within IRA rules |

| Recordkeeping | Maintains documentation for the account |

| IRS reporting | Supports the tax-advantaged structure of the IRA |

| Storage coordination | Connects the IRA to the approved depository arrangement |

That's why comparing custodians only on a headline annual fee can be misleading. One provider may look inexpensive at first glance, but another may provide clearer reporting, more transparent storage choices, or better account support.

The cost question to ask up front

A smart investor doesn't ask only, “What's the annual fee?”

The better question is, “What is the full first-year cost, including setup, annual administration, storage, and the premium paid to acquire the metals?”

For readers comparing providers side by side, this page to compare Gold IRA companies can help organize the research process.

Cost check: Fixed fees matter more in smaller accounts because they take up a larger share of the portfolio.

That doesn't make a Gold IRA wrong for a smaller investor. It just means the fee structure needs closer attention.

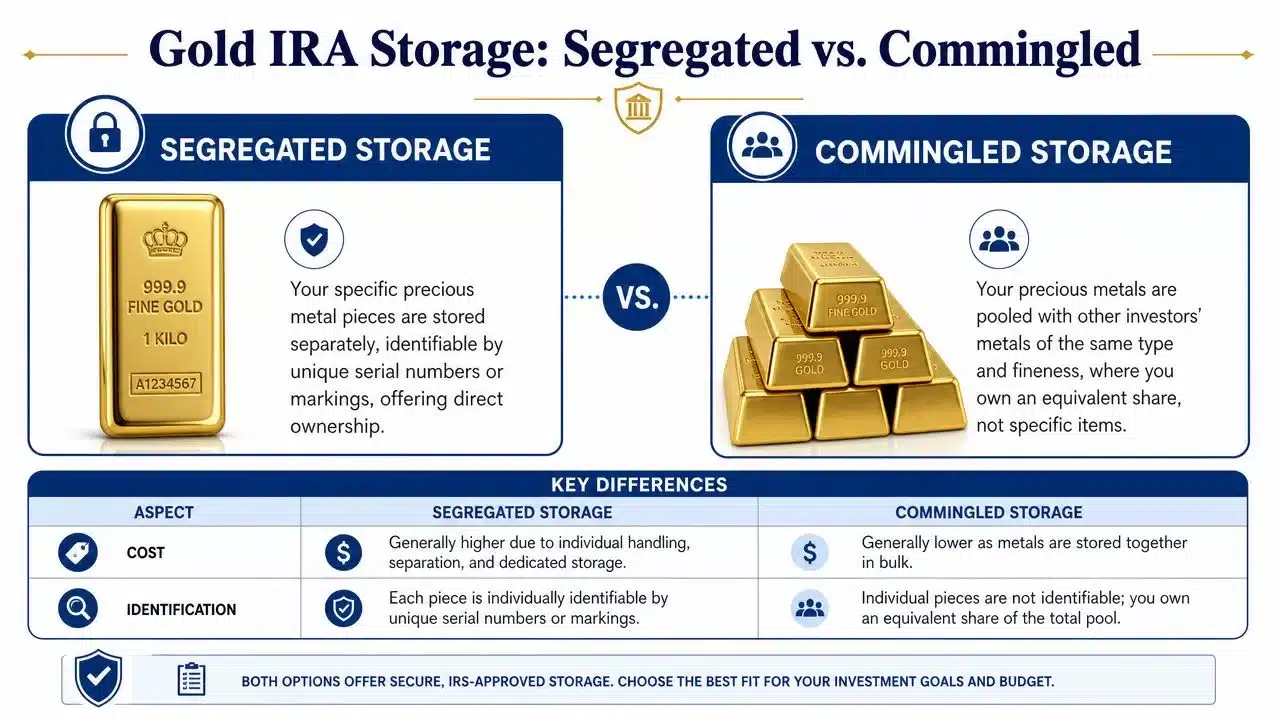

Segregated vs Commingled Storage What Custodians Offer

Storage is one of the least understood parts of a Gold IRA, and it's one of the most important. Most investors know the metals must go to an approved depository. Far fewer know they may have a choice in how those metals are stored.

That choice usually comes down to segregated or commingled storage.

What segregated storage means

With segregated storage, the investor's specific bars or coins are stored separately from other account holders' metals. The items are identifiable as that investor's holdings.

This option often appeals to people who want clarity around ownership, easier traceability, and a stronger sense that the exact assets purchased are the exact assets being held for them.

What commingled storage means

With commingled storage, metals are pooled with metals from other investors of the same type and fineness. Ownership is tracked at the account level rather than by isolating every specific item.

That doesn't automatically make commingled storage improper. It does mean the investor should ask more detailed questions.

According to this discussion of Gold IRA storage distinctions, many articles fail to explain the difference clearly, even though commingled storage can come with hidden costs or lower insurance limits, may reduce audit rights, and can increase the risk of loss if the depository fails.

A side-by-side view

| Storage type | General tradeoff |

|---|---|

| Segregated | Greater asset-specific identification and usually more transparency |

| Commingled | Pooled storage that may be simpler or less expensive, but can create questions about insurance, audits, and asset identification |

The key point isn't that one choice fits everyone. The key point is that this should be an explicit decision, not a buried default in account paperwork.

Questions worth asking the custodian

When discussing storage, investors should ask:

- Which depository is used and whether the name is disclosed in writing

- Whether the default option is segregated or commingled

- How insurance is described under each storage arrangement

- What records the investor receives showing what is held and how it is held

Some custodians make storage sound like a back-office detail. It isn't. Storage terms affect clarity, audit visibility, and the investor's comfort with the account.

For many near-retirees, this becomes a deciding factor. If two custodians look similar on price, the storage structure may reveal which one is more careful and transparent.

How to Choose a Reputable Gold IRA Custodian

Choosing an IRA custodian for gold becomes easier when the decision is reduced to a checklist. The strongest candidates aren't necessarily the ones with the loudest marketing. They're usually the ones that answer direct questions clearly and document everything in writing.

A short video can also help frame what to look for during the selection process.

Questions to ask before opening the account

- Is the custodian approved to handle this type of IRA? The answer should be straightforward, not vague.

- Can the full fee schedule be provided up front? That includes setup, annual administration, storage, and any transaction-related charges.

- What storage options are available? Ask directly whether segregated storage is offered and whether commingled storage is the default.

- Which depository is used? The name should be disclosed, along with information about insurance and reporting.

- How responsive is support? A near-retiree shouldn't have to chase basic answers about a retirement account.

- How are eligible metals screened? A careful process helps prevent ineligible purchases from entering the account.

Red flags that deserve caution

A few warning signs tend to show up early:

- High-pressure sales language instead of patient education

- Unclear or incomplete fees when asking for written disclosure

- Promises of guaranteed outcomes tied to gold ownership

- Loose answers about storage that avoid the segregated-versus-commingled question

- Blurry role definitions where the seller and custodian relationship isn't clearly explained

For readers who want a starting point for broader provider research, this page covering the top Gold IRA companies can help narrow the field.

Selection rule: If a custodian can't explain fees, storage, and compliance in plain language before the account is opened, it probably won't become clearer afterward.

Conclusion Your Next Step

A Gold IRA custodian does much more than hold paperwork. The custodian helps preserve compliance, screens for eligible metals, coordinates approved storage, and reduces the risk of mistakes that can turn a retirement account into a taxable event.

That's why the custodian deserves as much scrutiny as the metals themselves. For many investors, the most important choice isn't the coin or bar. It's the partner responsible for keeping the entire account on track.

A careful review of fees, storage structure, and compliance procedures can make the difference between a smooth retirement asset and an avoidable headache. This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.

Readers who want a low-pressure next step can explore Gold IRA Association to compare top Gold IRA companies, review educational guides, and continue researching custodians, storage options, and rollover rules before making a decision.