Many pre-retirees reach the same point at about the same time. The account balance looks substantial on paper, but inflation, market swings, and a heavy concentration in traditional assets start to feel less comfortable as retirement gets closer.

A 401k to Gold IRA rollover is one way to diversify part of those savings into physical precious metals inside a tax-advantaged retirement account. Done properly, it can be a clean administrative process. Done carelessly, it can create taxes, penalties, or even disqualify the account. This guide walks through the mechanics, the rules, and the long-term cost picture in plain English.

Why Consider a 401k to Gold IRA Rollover in 2026

For someone nearing retirement, the concern usually isn't chasing the highest possible return. It's protecting purchasing power and reducing the feeling that everything depends on the stock market behaving well at exactly the right time.

That's why physical gold comes up so often in retirement conversations. It isn't a magic solution, and it doesn't replace a full financial plan. But many savers view it as a diversification tool and a tangible asset that may help hedge against inflation and broader economic uncertainty.

Why this idea appeals to anxious but engaged investors

A typical pre-retiree often has a familiar mix of concerns:

- Inflation pressure: Everyday costs can rise faster than expected, which makes future withdrawal needs harder to estimate.

- Market volatility: A sharp downturn feels more serious when retirement is close and there may be less time to recover.

- Paper asset concentration: Many workplace plans are dominated by mutual funds, stock funds, and bond funds.

- Control and clarity: Some investors want part of their retirement savings tied to a physical asset held in a regulated depository.

Gold IRAs fit into that mindset because they allow retirement funds to hold IRS-approved physical bullion through a self-directed account structure. The appeal is less about speculation and more about balance.

Gold works best when it's treated as one component of a broader retirement strategy, not as an all-or-nothing bet.

What a rollover really does

A 401k to Gold IRA rollover doesn't mean stuffing coins into a home safe or cashing out a retirement plan. It means moving eligible retirement funds from a 401(k) into a self-directed IRA that can hold approved precious metals under IRS rules.

That distinction matters. The structure stays within the retirement system. The account remains tax-advantaged if the rollover is handled correctly, the metals meet eligibility rules, and storage follows IRS requirements.

For many readers, the true value of this option is psychological as much as financial. It offers a way to take action instead of merely hoping inflation cools, markets stay calm, and retirement timing lines up perfectly.

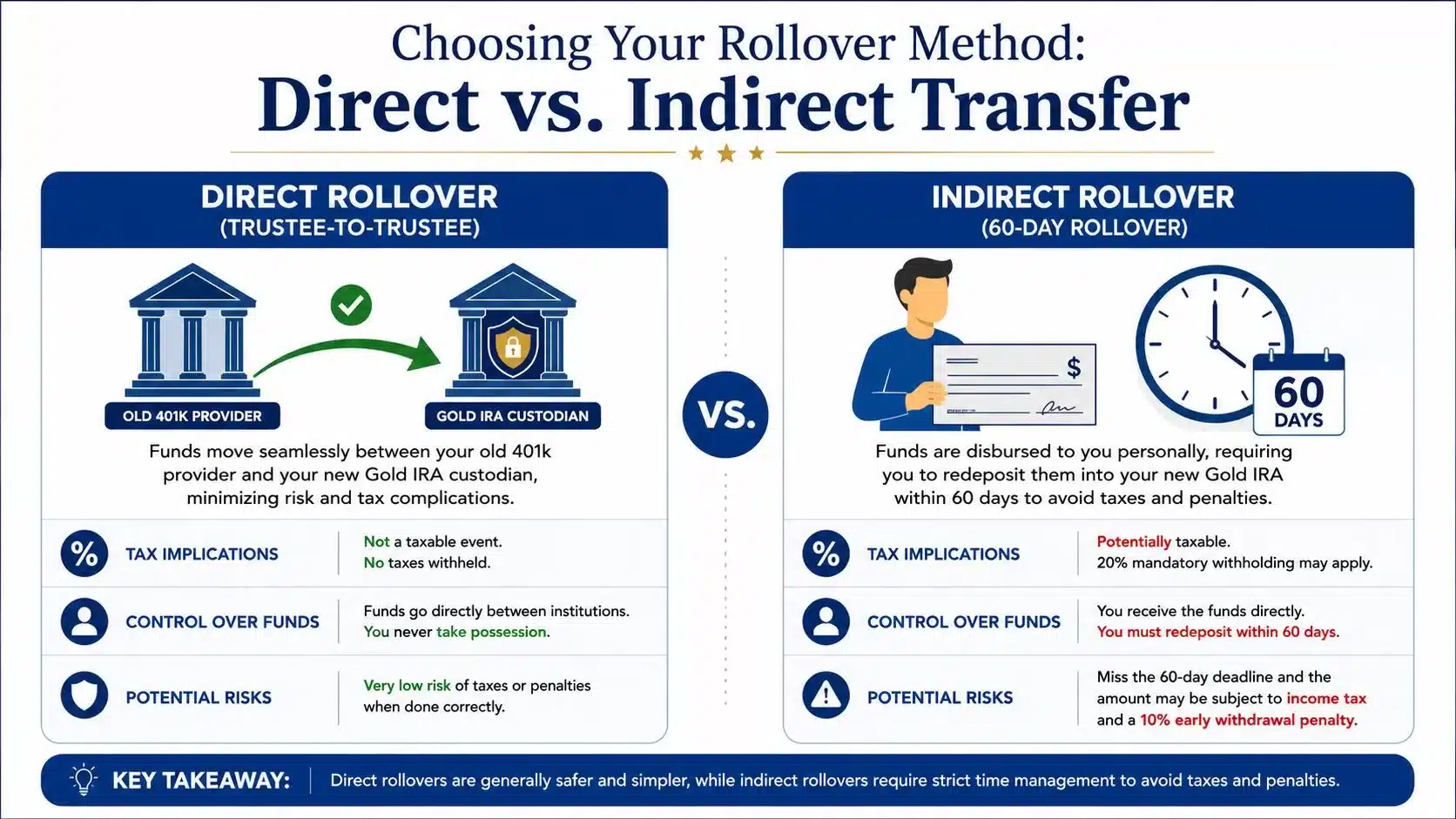

Choosing Your Rollover Method Direct vs Indirect Transfer

A lot of rollover mistakes start here. Two methods can both be called a rollover, but they do not carry the same level of tax risk, timing pressure, or administrative burden.

The easiest way to separate them is by asking one question: Does the money ever touch your hands? If the answer is no, the process is usually cleaner. If the answer is yes, your responsibilities increase fast.

Direct rollover

A direct rollover, also called a trustee-to-trustee transfer, sends funds from the old 401(k) plan straight to the new Gold IRA custodian. The account owner does not receive the money personally.

For many pre-retirees, this works like handing a package from one licensed carrier to another instead of taking it home and trying to re-ship it yourself. There are fewer chances for delay, fewer chances for paperwork errors, and less risk of accidentally creating a taxable event.

Direct rollovers are usually the preferred method for a 401(k) to Gold IRA move because the funds stay inside the retirement system during the transfer. That reduces the chance of running into the 60-day redeposit rule that applies to indirect rollovers.

It also matters from a long-term cost perspective. A direct rollover does not erase Gold IRA fees, but it can help you avoid preventable taxes or penalties that would raise your 10-year total cost of ownership before the account is even fully set up.

Indirect rollover

An indirect rollover means the distribution is sent to you first. You then have to deposit those funds into the new IRA within the IRS time limit.

This is the option that sounds manageable on paper and becomes risky in real life.

A check can sit in the mail. A bank can place a hold on deposited funds. A form can be filled out incorrectly. A deadline can be misunderstood. Any one of those problems can turn a planned rollover into a taxable distribution, and if you're under the eligible age threshold, that can also trigger an early withdrawal penalty.

The pressure is not just legal. It is practical. You become the traffic cop, recordkeeper, and deadline manager for money that is supposed to stay sheltered for retirement.

Readers who want a fuller walkthrough of the rules and paperwork can review how to move a 401k to gold without penalty.

Practical rule: If your plan allows a direct rollover, that is usually the lower-risk choice.

Direct vs. Indirect Rollover Comparison

| Feature | Direct Rollover (Trustee-to-Trustee) | Indirect Rollover (60-Day) |

|---|---|---|

| How funds move | Funds move directly between institutions | Funds are paid to the account holder first |

| Tax risk | Lower when handled correctly | Higher if the redeposit is late or mishandled |

| Penalty exposure | Lower because the account holder does not take possession of funds | Higher if the 60-day deadline is missed |

| Paperwork burden | Usually handled more efficiently between custodians and plan administrators | Requires close personal tracking and follow-up |

| Best fit | Most rollover situations | Limited cases where direct movement is not available |

A common point of confusion

Some investors hear "indirect" and assume it offers more control. In reality, it often creates more ways to make an expensive mistake.

Direct rollover keeps the transfer inside the retirement framework. Indirect rollover places the timing, documentation, and redeposit burden on you. For someone comparing Gold IRA costs over the next decade, that distinction matters. One administrative error at the start can outweigh years of careful fee shopping.

The Step-by-Step Rollover Process Explained

A rollover often feels stressful at the start for one simple reason. You are moving retirement money from a familiar account into a structure with stricter rules, new paperwork, and more than one institution involved.

The good news is that the process is usually straightforward once you see the order of operations. The key is to treat it like a relay race. Each party has one job, and problems tend to happen only when the handoff is unclear or done out of order.

Step 1 Choose a self-directed IRA custodian

A regular brokerage IRA usually does not support physical precious metals. You need a self-directed IRA custodian that can hold alternative assets and handle the reporting rules tied to IRA-owned bullion.

Slow down here.

A good custodian does more than open the account. It should be able to explain the paperwork in plain English, coordinate with the old plan administrator, and show you how storage, transaction, and annual account fees work over time. That long-view cost discipline matters. A rollover that looks inexpensive in year one can become far more costly over 10 years if the account carries high annual fees or wide metal markups.

Step 2 Open the new Gold IRA before any money moves

The receiving account has to exist before your 401(k) administrator can send funds to it. That means completing the application, naming the account correctly, and getting the new custodian's transfer details ready first.

If you want a closer look at the paperwork sequence, review this guide on how to move 401k to gold without penalty.

Step 3 Submit the rollover request to the old plan

After the new IRA is open, you authorize the old 401(k) plan to send the funds to the new custodian. In a direct rollover, the money stays inside the retirement system the whole time, which is why many investors prefer it.

The usual order is simple. Choose the custodian, open the account, complete the rollover request, wait for the transfer to arrive, submit the purchase instructions for approved metals, and confirm delivery to an approved depository. Seeing those steps in order helps reduce a lot of the anxiety around the term "rollover."

Step 4 Wait for the cash transfer to clear

This stage tests patience.

Your current 401(k) investments may need to be sold first, with the proceeds then sent to the new IRA custodian. That can take time, especially if the plan administrator has internal review steps or mailing procedures.

A short video overview can help make the process feel less abstract:

Delays do not automatically signal a problem. They often reflect the normal mechanics of liquidation, transfer processing, and account funding.

Step 5 Direct the IRA to buy eligible metals

Once the cash reaches the new account, you do not personally buy coins and drop them into the IRA. The purchase has to run through the IRA itself.

In practice, that means you submit an investment direction form telling the custodian what IRS-eligible metals to purchase. The custodian then carries out the transaction within the IRA structure. This distinction is easy to miss, but it matters. Personal possession or off-process purchases can create compliance problems that are expensive to fix.

It also affects long-term cost. The metals you select, the premium paid over spot, and the account's trading process all shape your 10-year total cost of ownership, not just the setup fee.

Step 6 Confirm storage and keep the records

After the purchase, the metals are shipped to an approved depository, checked in, and recorded under the IRA. You should receive documentation showing the asset type, quantity, and storage location.

The rollover is complete only after the IRA buys approved metals and those metals are stored through the required custodial process.

One more issue for current employees

Old 401(k) plans are often easier to move than active workplace plans. If you still work for the employer sponsoring the plan, the plan document controls whether you can move money out while still employed.

Ask the plan administrator one direct question: does the plan allow an in-service rollover to a self-directed IRA?

That wording matters. A request can get delayed if the administrator is unclear about the destination account or assumes you are asking for a taxable withdrawal. Confirm eligibility before opening a file of forms, and confirm it again before any assets are sold.

What Metals Are Eligible for a Gold IRA

You complete the rollover, fund the new IRA, and feel ready to buy gold. Then the first real fork in the road appears. The coin or bar that looks right to you is not always the one the IRS allows inside a retirement account.

That catches many careful investors off guard.

A Gold IRA follows a narrower rulebook than a personal precious metals purchase. The account is generally limited to certain forms of bullion that meet IRS purity standards and move through the custodian to an approved depository. If a metal fails one of those tests, the problem is not cosmetic. It can affect the account's tax treatment and create costs that linger for years.

The purity rules that matter

The IRS sets minimum fineness standards for precious metals held in an IRA. In practice, that means the metal must be refined to a high enough purity level before it can qualify.

The general thresholds are:

- Gold: 99.5% pure or higher

- Silver: 99.9% pure or higher

- Platinum: 99.95% pure or higher

- Palladium: 99.95% pure or higher

- Exception: The American Gold Eagle is permitted even though it is 91.67% pure

That exception confuses many readers. A simple way to look at it is this: IRA rules are mostly based on purity, but a small number of products are specifically allowed by statute. So the purity rule is the starting point, not the only rule.

What usually qualifies

Gold IRA eligibility usually points investors toward bullion products made for metal ownership, not rare-coin collecting.

Items that generally fit the rules include:

- Bullion coins and bars that meet the required fineness

- Products the IRA custodian can purchase for the account

- Metals shipped directly to an approved depository

The key idea is standardization. IRA-approved metals are usually easy to verify, easy to price, and easy for the custodian and depository to document. That matters for compliance, and it also matters for your 10-year cost picture because products with higher dealer premiums can raise your total ownership cost long after the rollover is finished.

What usually does not qualify

Some products create problems even if they contain real precious metal.

These are commonly excluded or risky for IRA use:

- Collectible coins

- Jewelry

- Numismatic pieces

- Metals bought personally and then sent in later

- Anything kept at home, in a safe, or in a personal lockbox

A helpful rule of thumb is that retirement accounts are built for approved investment bullion, not for memorabilia or personal possession.

Why storage is part of eligibility

Eligibility is not only about what you buy. It is also about where it is held.

For IRA purposes, the metals must be stored through an approved depository under the account's custodial arrangement. If an investor takes personal possession, the IRS can treat that move as a distribution rather than a protected IRA holding. That can mean taxes, penalties, or both, depending on the situation.

Readers who want a broader overview of approved products, custody requirements, and related restrictions can review these IRS rules for precious metal IRAs.

One final point often gets missed. Metal choice affects cost, not just compliance. A bar or coin with a larger markup over spot may still be eligible, but over a long holding period that premium becomes part of the account's total cost of ownership. That is why a good Gold IRA decision starts with "Is it allowed?" and quickly moves to "What will this choice cost me over 10 years?"

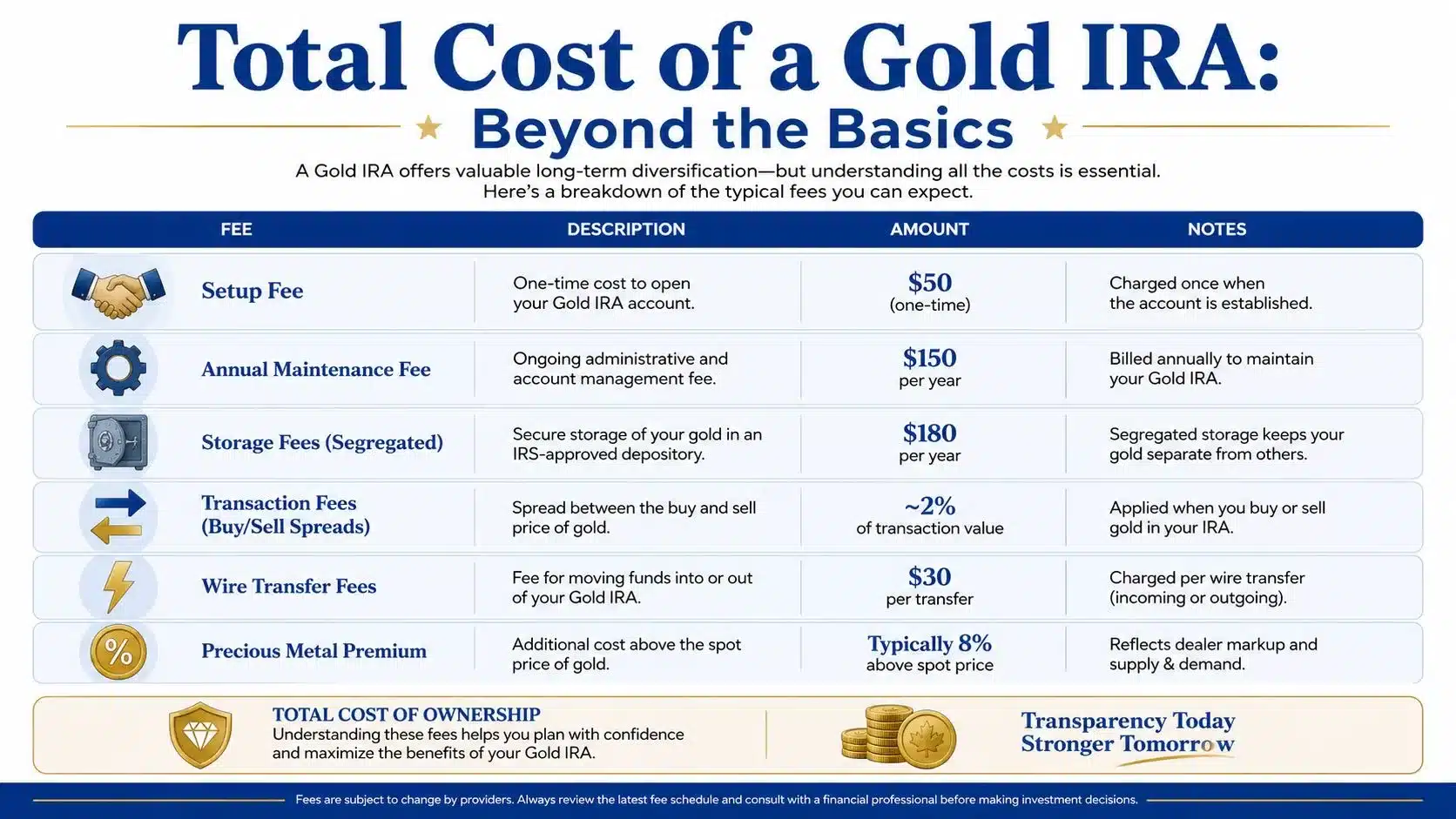

Understanding the Total Cost of a Gold IRA

A pre-retiree rolls $50,000 from a 401(k) into a Gold IRA and sees a setup fee that looks manageable. A year later, the account also has custodial charges, storage costs, insurance fees, and the markup paid when the metals were bought. None of those costs is shocking by itself. The surprise comes from what they add up to over 10 years.

The long-term cost picture

Gold IRA costs make more sense if you view them the way you would view the total cost of owning a house or a car. The purchase price matters, but the ongoing expenses shape the actual long-term outcome.

For a Gold IRA, that means looking beyond the opening paperwork and asking a better question: what will this account likely cost to own over a decade? For many investors, that 10-year view is more useful than a single annual fee quote because retirement money is usually held for years, not briefly.

A Gold IRA can still make sense for someone who wants physical precious metals inside a tax-advantaged account. The point is to judge it with the full cost visible, not just the first bill.

Where the costs usually come from

Gold IRA pricing usually comes in layers:

- Initial setup fees: often a one-time charge to open the account

- Annual custodial charges: the cost of account administration and reporting

- Storage and insurance fees: charges for holding the metals in an approved depository

- Transaction spreads: the difference between the market price of the metal and the dealer's buy or sell price

Transaction spreads are the part many readers miss. If you buy metals at a premium over spot and later sell at a discount to spot, that gap functions like a hidden ownership cost. It may not appear on the account statement as a line item, but it still affects your return.

That is why a 10-year total cost of ownership view matters so much.

Why these costs feel different from a regular retirement account

A traditional 401(k) or a standard IRA invested in mutual funds can have costs that stay mostly in the background. A Gold IRA is different because custody and storage are built into the structure itself. You are not only paying for an investment. You are also paying for a compliant system to hold physical metal under IRS rules.

That distinction helps explain why fee comparisons can feel confusing. An investor may compare a Gold IRA to a low-cost index fund and assume the economics will be similar. They usually are not. The two account types solve different problems and carry different operating costs.

How to judge whether the cost is reasonable

Start with the role gold is supposed to play in your retirement plan. If the goal is diversification and inflation hedging, then the question is whether the expected benefit justifies the long-term carrying cost.

A simple way to test that is to estimate 10 years of ownership, not just year one. Add the setup fee, projected annual custody and storage charges, and the likely purchase and sale spread. Then compare that total with the size of the rollover and the reason you want metals in the first place.

Readers who want a category-by-category breakdown can review this Gold IRA rollover fees guide with setup, storage, custodian, and spread costs explained.

A good Gold IRA decision is rarely about a single fee. It is about whether the full decade-long cost fits the job you want the account to do.

Critical Mistakes to Avoid During Your Rollover

A common rollover story goes like this: the account gets opened, the money leaves the 401(k), the metals are purchased, and only afterward does the investor learn that one paperwork choice or storage decision may have created a tax problem.

That is why the most expensive rollover mistakes are often administrative, not market-related. The price of gold can rise or fall. A compliance error can trigger taxes, penalties, delays, or even a failed rollover structure.

The biggest mistake is improper storage

Physical gold inside an IRA has to be held through an approved custodian and stored at an approved depository. Personal possession is the line many people misunderstand. If the metals are sent to your house, safe, or personal box, the IRS can treat that as a distribution rather than compliant IRA storage under IRC §408(m).

That matters because the tax hit can be immediate. If the account is disqualified, the value can become taxable in the year of the mistake, and early distribution penalties may also apply for those who are under the applicable age threshold.

The same problem can happen with the wrong coins or bars. Some products that look like sensible gold purchases do not qualify for IRA use. Collectibles are the classic trap.

Other rollover errors that cause trouble

A rollover works a lot like a relay race. If one handoff goes wrong, the rest of the process can still be affected.

- Choosing an indirect rollover without understanding the clock: With an indirect rollover, the funds are paid to you first, and the redeposit deadline becomes your responsibility. Missing that window can turn a rollover into a taxable event.

- Buying metals before the IRA is fully set up: The account structure has to come first. If the metal purchase happens outside the IRA and gets moved later, the transaction may not be treated the way the investor expected.

- Using a provider who does not regularly handle precious metals IRAs: Standard IRA paperwork and precious metals IRA paperwork are not identical. Small processing errors can cause delays at the exact moment timing matters.

- Rolling over too much at once: Gold can serve a diversification role, but concentration risk is still risk. A hedge should not create a new imbalance in the retirement plan.

- Focusing only on year-one fees: A rollover can look reasonable at the start and still turn out costly over a decade. Setup fees, annual custody charges, storage costs, and buy-sell spreads need to be judged together, especially if the rollover amount is modest.

That last point gets missed often.

An investor may work hard to avoid a tax mistake and still make an expensive economic mistake by ignoring 10-year ownership costs. If two rollover options look similar on day one, the better choice is usually the one that still makes sense after years of storage and administrative fees, not just the one with the lower opening charge.

The most damaging mistakes usually begin as casual assumptions. "I'll store it temporarily" or "this coin should qualify" can create consequences that are much larger than they sound.

A good final check

Before authorizing the rollover, make sure you can answer these four questions without hesitation:

- Is the account a self-directed IRA set up to hold physical precious metals?

- Is the transfer being handled directly, if that option is available?

- Are the specific coins or bars eligible under IRS rules?

- Will the metals go straight to an approved depository rather than to personal possession?

If any answer is unclear, pause and verify it before money moves. A short delay is usually cheaper than fixing a rollover mistake after the fact.

Frequently Asked Questions About 401k to Gold IRA Rollovers

Can a current employer 401(k) be rolled into a Gold IRA?

Sometimes. It depends on whether the plan allows an in-service rollover. Some plans permit it, especially for older participants, while others don't. The fastest way to find out is to ask the plan administrator for the relevant distribution rules in the current plan documents.

How much of a 401(k) should go into gold?

There isn't a universal answer. That's an asset-allocation decision based on risk tolerance, retirement timeline, other holdings, and personal goals. A Gold IRA can play a diversification role, but concentration in any single asset class deserves careful thought.

What happens when distributions begin?

Distributions from a Gold IRA follow the rules of the underlying IRA type and the investor's circumstances. Some account holders sell metals within the account and take cash distributions. Others may be able to take distributions in kind, meaning the metals themselves are distributed. Tax treatment can vary, so this is a good place for individualized tax guidance.

Can money be added after the initial rollover?

In many cases, yes. Investors may be able to fund the account further through eligible transfers, rollovers, or contributions, depending on the account structure and current IRS rules. Those rules can change, so current guidance should be verified before acting.

Is a 401k to Gold IRA rollover hard to do?

It's more procedural than difficult. The main challenge is not complexity for its own sake. It's making sure each administrative and IRS rule is handled in the right order. Most anxiety comes from unfamiliar terminology, not from impossible steps.

A 401k to Gold IRA rollover can make sense for investors who want physical precious metals as part of a broader retirement strategy. The key is understanding the mechanics, respecting the storage and eligibility rules, and judging the decision by its long-term ownership cost, not just by the appeal of gold itself.

This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.

Gold IRA Association publishes reader-first education for pre-retirees who want to understand rollover rules, eligible metals, fees, and provider selection without the hype. For a practical next step, readers can compare top Gold IRA companies at Gold IRA Association or talk through questions with a specialist at 888-910-8386.