A lot of pre-retirees reach the same point. They've built most of their retirement savings in mutual funds, stocks, or bond-heavy accounts, but they don't love having everything tied to paper assets and market sentiment. A self directed Gold IRA can look like a practical way to add something tangible, but the rules are stricter than many people expect.

This guide walks through how a self directed Gold IRA works, what metals qualify, how rollovers usually happen, where investors get tripped up on storage, and how to think about fees without hype. It also covers two issues many articles gloss over: the tax danger of “home storage” setups and the actual tradeoff between segregated and commingled storage.

What Is a Self-Directed Gold IRA?

A pre-retiree rolls money from an old 401(k) into a new Gold IRA, buys bullion, and assumes the hardest part is over. Then a salesperson mentions an IRA-owned LLC and "home storage" as a way to keep the coins close at hand. That is the point where a useful retirement tool can turn into a compliance trap.

A self directed Gold IRA is an Individual Retirement Account that can hold certain physical precious metals within the IRA structure, rather than limiting you to standard brokerage assets. The account is still a retirement account with tax rules, contribution rules, rollover rules, and custody requirements. What changes is the investment menu and the amount of responsibility placed on the account owner to choose approved assets and follow the handling rules carefully.

The term "self-directed" causes a lot of confusion. It does not mean you become your own IRA custodian or store IRA metals in your house. It means you direct the investment choices, while a specialized custodian administers the account and an approved depository holds the metal. If you want a plain-English overview of those self-directed precious metal IRA rules, start there before evaluating any sales pitch.

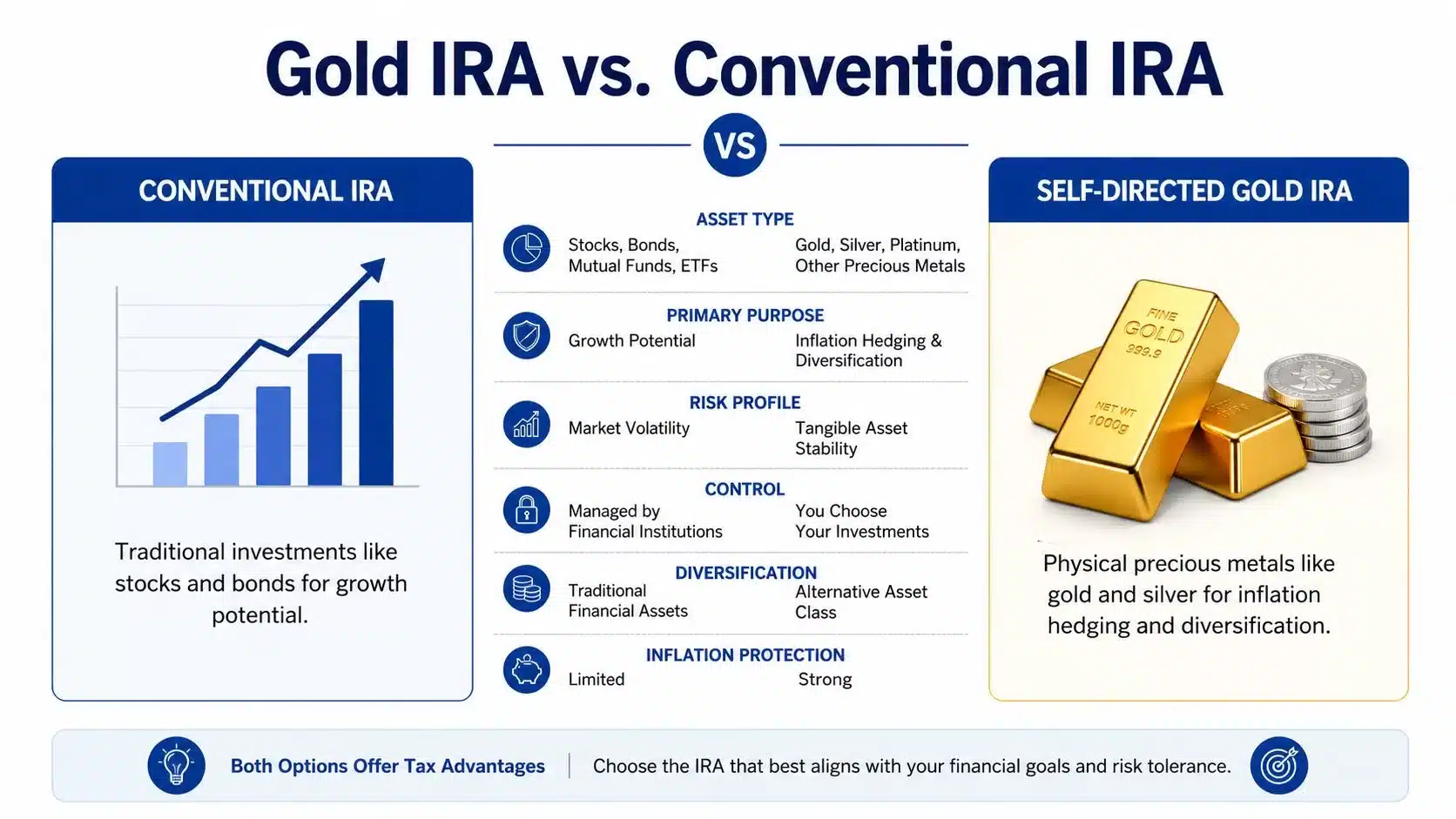

How it differs from a conventional IRA

A conventional IRA usually holds financial assets such as mutual funds, stocks, bonds, ETFs, and cash equivalents. A self directed Gold IRA uses the same tax-advantaged account framework, but part of the account can be allocated to approved forms of gold and, in many cases, other permitted precious metals.

In practice, that means your retirement savings may include a physical asset layer instead of only paper claims tied to markets, issuers, or fund managers. Some investors like that added tangibility. Others underestimate the extra administration that comes with it.

The metal is bought for the IRA, titled to the IRA, and stored for the IRA. That separation matters.

Why investors consider one

Many pre-retirees look at a Gold IRA as a diversification tool, not as a replacement for the rest of a retirement plan. The goal is often to hold one asset class that behaves differently from stocks or bonds, while keeping the tax treatment of an IRA.

That said, owning bullion inside an IRA is not the same as buying coins personally. Personal ownership gives you direct possession and fewer retirement-account rules. IRA ownership gives you tax advantages, but it also brings custodial oversight, storage fees, reporting requirements, and strict limits on how the metal is held.

This is also where many articles stay too general. The key decision is not just "gold or no gold." It is whether the benefits of holding physical metal inside a retirement account outweigh the ongoing costs and the narrower compliance lane.

The hidden complexity many buyers miss

The biggest misunderstanding is storage. Some promoters present "home storage" or IRA-LLC arrangements as a shortcut that lets you control the metal directly while keeping IRA tax treatment. Investors should treat that claim with caution. If the arrangement fails IRS scrutiny, the account can be treated as a distribution, which may create current taxes and possible penalties.

A safer starting assumption is simple. If metals are owned by the IRA, the account owner should not keep them in a home safe, safe-deposit box, garage, or personal vault.

There is a second complexity that matters in practice: storage format. Once investors accept that approved depository storage is part of the deal, they still need to compare segregated storage and commingled storage. Segregated storage usually means your specific coins or bars are kept separate from other clients' holdings, which can provide more precision in recordkeeping but often costs more. Commingled storage usually means your holdings are stored with like assets of other IRA owners, which may reduce fees but offers less item-by-item separation. The right choice depends on account size, product type, and whether the extra cost buys peace of mind you value.

A self directed Gold IRA can serve a clear purpose in a retirement plan. It just works best when you view it as a regulated account with physical assets, not as a loophole for private possession.

IRS Rules for Eligible Gold and Precious Metals

A common mistake happens before any metal is purchased. An investor sees a well-known coin, assumes "gold is gold," and later learns the IRA cannot hold it. In this part of the process, small wording differences matter because the IRS draws a line between approved bullion and products treated as collectibles.

Under this explanation of IRA-eligible precious metals, Internal Revenue Code Section 408(m)(3) sets fineness standards for bullion that can be held in an IRA. The practical point is simple. IRA eligibility depends on the metal's purity and on whether the product fits the IRS rules for approved bullion.

The purity rules investors need to know

The baseline standards are:

- Gold: at least 99.5% pure

- Silver: at least 99.9% pure

- Platinum: at least 99.95% pure

- Palladium: at least 99.95% pure

Those numbers are the first filter, not the only filter. A product can contain precious metal and still fail IRA rules if it is treated as a collectible or does not come from an acceptable source. That is why a retirement account should be handled more like a regulated inventory system than a personal coin collection.

The exception that causes confusion

One coin trips up many careful buyers: the American Gold Eagle. It is 91.67% pure, which is below the usual gold standard, yet it is still allowed in an IRA because the statute specifically permits it.

That exception is narrow. It does not open the door for other 22-karat coins. A useful way to read the rule is this: the IRS framework has a general purity test, and then a few products pass because the law names them specifically.

What usually qualifies, and what usually creates trouble

Products that generally fit the rules are bullion coins and bars made for metal investment, not collector appeal. Products that often create problems are rare coins, graded coins, proof sets sold mainly for numismatic value, and items priced far above their melt value.

A simple screening process helps:

- Check fineness first. If it misses the purity threshold, the IRA usually cannot buy it.

- Check whether it is bullion or a collectible. Marketing language often gives this away.

- Check the producer. Recognized government mints and approved refiners are usually the safer lane.

- Check before money leaves the account. Undoing a non-eligible purchase can create delays, fees, and tax reporting issues.

This is one of the hidden complexities many articles gloss over. Product eligibility sounds like a shopping question, but it is really a compliance question. If a dealer pushes "special" coins with high premiums, the safer response is to ask whether the item is IRA-eligible and to get that confirmed by the custodian before purchase.

Readers who want a more detailed list of precious metal IRA rules and eligible product categories can review that guide.

How to Set Up an Account and Fund It via Rollover

The setup process is manageable when it's viewed as a sequence. Confusion usually comes from trying to think about custodians, funding, and metal selection all at once. In practice, most investors move through it in three stages.

Step one starts with the account structure

First, the investor opens a self-directed IRA with a custodian that supports precious metals. At this stage, the focus isn't on buying coins yet. It's on getting the legal account framework in place so retirement money has somewhere compliant to go.

Individuals considering this route are funding it in one of two ways:

- A new annual contribution

- A rollover or transfer from an existing retirement account

For a broader walkthrough, this Gold IRA rollover guide is useful when evaluating the mechanics.

Funding usually matters more than product selection

Once the account is open, the next decision is how money gets into it. For this process, readers often hear the terms direct rollover and indirect rollover.

A direct rollover generally means funds move from one retirement account institution to another without the investor taking possession of the money. That tends to be the cleaner path from a compliance standpoint.

An indirect rollover generally means the money is paid out first and then has to be redeposited into the retirement account according to IRS rules. This can be where avoidable tax issues arise if the timing or paperwork goes wrong.

For most retirees, simpler is better. If a trustee-to-trustee movement is available, that usually reduces room for error.

Here's a quick visual summary of the setup flow:

The purchase happens after the account is funded

Only after the account is funded does the investor direct the purchase of approved metals. At that point, the custodian coordinates the transaction and the metals are sent to the approved storage facility, not to the investor's home.

That sequence matters:

- Open the account first

- Fund it through contribution, transfer, or rollover

- Select approved metals

- Have the IRA purchase and store them properly

A common mistake is thinking personally owned gold can be dropped into the IRA later. That isn't how these accounts are typically structured. The IRA needs to acquire eligible assets through the account process itself.

Where paperwork errors usually happen

Most setup delays come from ordinary administrative issues, not from the metal itself. Missing account forms, unclear rollover instructions, incomplete beneficiary designations, or mismatched names across retirement accounts can slow things down.

A careful investor usually asks three questions before signing anything:

- Who is the custodian handling the IRA administration?

- How is the rollover or transfer being documented?

- Which approved metals will the IRA purchase once funds arrive?

Those questions keep the process grounded in compliance instead of marketing.

Choosing a Custodian and Secure Storage

A lot of confusion starts here. An investor finishes the rollover paperwork, picks the coins or bars, and assumes the hard part is over. In practice, this is the stage where small misunderstandings can create expensive mistakes, especially around who controls the metal and where it is allowed to sit.

A self directed Gold IRA usually involves two separate firms with two separate jobs. The custodian handles the IRA itself. The depository handles the metal. If those roles get blurred together, it becomes harder to compare fees, verify responsibility, and spot risky marketing claims.

IRS rules generally require IRA-owned precious metals to be held by a qualified trustee or custodian, not by the account owner personally. In plain English, the gold belongs to the IRA, so it has to stay inside the IRA's custody chain. The same basic rule is why the popular "home storage" pitch deserves extra scrutiny. If an arrangement is marketed as letting you keep IRA gold in your house, safe, or personal lockbox through an IRA-LLC structure, that is a compliance trap. If the IRS treats the metals as distributed to you, the account can lose its tax-advantaged status and trigger taxes and penalties.

What the custodian does and what the depository does

The custodian is the IRA administrator. This party usually handles:

- Account records

- IRS reporting

- Transaction processing

- Required administrative oversight

The depository is the vaulting facility. This party usually handles:

- Receiving the metals

- Secure storage

- Inventory tracking

- Release procedures when metals are sold or distributed

That division matters. A sales representative may describe the process as if one company does everything, but investors should know exactly which firm is responsible for paperwork and which one is responsible for physical control.

If you want a clearer framework for vetting account administrators, this guide on choosing an IRA custodian for gold is a useful starting point.

The home storage IRA-LLC trap

This issue gets less attention than it should.

Some promoters frame an IRA-owned LLC as a shortcut to personal control. The pitch often sounds simple: your IRA owns an LLC, the LLC buys gold, and you store it yourself as manager of that LLC. The problem is that legal control and physical possession are not the same thing. IRS rules around prohibited transactions and constructive receipt are strict, and a setup that gives you direct personal possession can invite the argument that the IRA assets were distributed or used for your personal benefit.

That is not a minor paperwork problem. It can mean ordinary income tax on the distributed amount, early withdrawal penalties if you are under the applicable age threshold, and loss of the IRA's intended tax treatment. A careful investor treats any promise of easy at-home possession as a warning sign, not a convenience.

Commingled and segregated storage are different choices

Once the custody issue is clear, the next decision is how the metals are stored inside the depository. The two common options are commingled and segregated storage.

| Storage type | How it works | Best fit |

|---|---|---|

| Commingled | Your metals are stored with the same type of metals belonging to other IRA account holders | Investors who want lower ongoing storage costs |

| Segregated | Your specific bars or coins are stored separately and identified to your account | Investors who want item-level separation |

The practical difference is similar to airport baggage versus a private checked case. In both situations, your property is tracked and returned to you. The question is whether you want your exact items kept apart the whole time, and whether that added separation is worth the higher annual cost.

How to judge the cost-benefit tradeoff

Bigger accounts often justify more scrutiny here.

Commingled storage usually costs less and works well for investors who care more about broad precious-metals exposure than about receiving the exact same coins or bars later. Segregated storage usually costs more, but it gives clearer item-specific identification, which some investors value for recordkeeping, peace of mind, or large concentrated holdings.

Ask direct questions before you agree to either option:

- Will my account hold exact identified bars or coins, or equivalent like-kind metals?

- How is inventory documented and audited?

- How is insurance described in the storage agreement?

- What event triggers extra fees, such as shipping, liquidation, or in-kind distribution?

Insurance language deserves special attention. Some depositories describe coverage at the facility or accounting level rather than as a simple promise tied to one investor's exact coin tube or bar number. That does not automatically make commingled storage a bad choice. It does mean the lower-cost option should be chosen with clear eyes.

A careful investor is not only buying gold. The investor is also buying a custody process, a documentation trail, and a storage arrangement that needs to hold up if the IRS ever asks questions.

Understanding the Fees and Tax Implications

A lot of investors focus on the price of the gold and underestimate the price of the wrapper around it. With a self directed Gold IRA, the account structure, custody rules, and storage requirements often cost as much attention as the metal itself.

That matters because fees reduce returns every year, while tax mistakes can trigger a much larger hit all at once.

A neutral overview from ConsumerAffairs notes that Gold IRA investors commonly face a setup charge, ongoing account administration fees, and separate storage costs. In plain terms, you are paying for three different jobs: someone to administer the IRA, someone to hold title and keep records, and someone to store the bullion in an approved facility.

The main fee buckets

Most accounts have three core cost categories:

- Setup fee: A one-time charge to open the IRA and process the paperwork

- Annual administrative fee: Ongoing custodian charges for reporting, recordkeeping, and compliance

- Storage fee: Depository charges for holding and insuring the metals

Some providers also add transaction fees for purchases, sales, wire transfers, account termination, or taking metals out of the vault. Such additional charges often surprise investors. A quoted annual fee can sound reasonable until the smaller line items start stacking up.

A practical way to judge cost is to ask for a full fee schedule in writing and read it like a closing disclosure on a house. The headline number rarely tells the whole story.

Contribution limits for 2026

A self directed Gold IRA follows the same annual contribution rules as other IRAs. It does not get a special higher limit because the account holds bullion.

For current annual IRA contribution limits, use the official IRS retirement topics and publications rather than a dealer summary. The IRS updates those figures when limits change, and that is the cleanest source for year-specific numbers.

Tax treatment in plain English

The tax treatment depends first on whether the account is structured as a traditional IRA or a Roth IRA. Traditional IRA contributions may be deductible in some cases, and withdrawals are generally taxed later. Roth IRA contributions are generally made with after-tax dollars, and qualified withdrawals are generally tax-free.

The key point is simpler than the jargon. The tax advantage belongs to the IRA, not to the gold itself. If the account breaks IRA rules, the IRS can treat the metals as distributed to you personally.

That is why the so-called home storage arrangement deserves extra scrutiny. Some promoters package an IRA-owned LLC and suggest that this gives the investor direct physical control over the coins or bars. The trap is that personal possession can be treated as a distribution if the structure fails IRS requirements. If that happens, the value may become taxable in the year of the violation, and early-withdrawal penalties may also apply if the account owner is below the applicable age threshold.

A safe rule of thumb is this: if the setup leaves you holding IRA metals at home, in a personal safe, or in a safe deposit box under your direct control, stop and get a tax opinion from a qualified CPA or tax attorney before proceeding.

A few practical reminders help keep the tax side clear:

- Contributions follow normal IRA rules: Income limits, deduction rules, and annual caps still apply

- Rollovers and transfers need careful handling: A mistake in timing or paperwork can create a taxable event

- Distributions are reportable: Cash withdrawals and in-kind distributions of metals both have tax consequences

- Possession matters: Personal control of IRA metals can create a compliance problem, especially in home storage arrangements

Fees are a nuisance. Compliance errors are more serious. A good self directed Gold IRA decision weighs both, because the cheapest-looking setup can become the most expensive if it cuts corners on custody or storage rules.

This is not financial or tax advice. Investors should review account documents carefully and speak with a licensed financial advisor, CPA, or tax professional before acting.

Pros, Cons, and How to Mitigate Risks

A self directed Gold IRA often looks simple from a distance. You buy gold inside a retirement account and hold it for the long term. In practice, it works more like owning a rental property inside an IRA than buying a stock fund. The asset may be familiar, but the rules, handling, and costs are much more specialized.

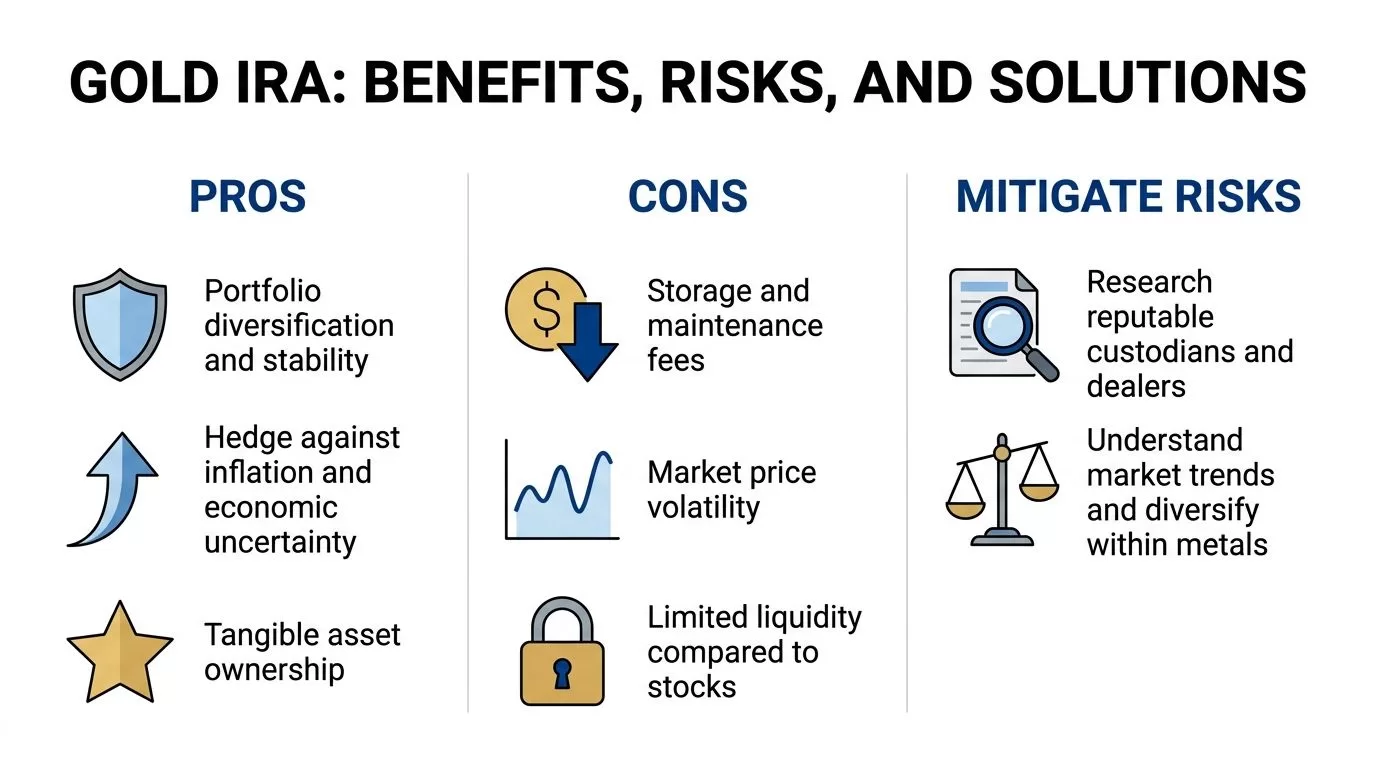

The upside is clear enough. Gold can give a retirement portfolio exposure to a physical asset that does not behave exactly like stocks or bonds. Some investors also like the discipline of owning bullion through a tax-advantaged account instead of trading in and out based on headlines.

The limitations matter just as much.

Physical bullion does not produce income. The account also adds custody, storage, paperwork, and product-selection rules that do not exist in a plain vanilla IRA. That means a Gold IRA has a higher hurdle to justify itself. The account has to earn its place in the portfolio despite the extra friction.

Where a Gold IRA can add value

A Gold IRA may fit an investor who wants to broaden retirement holdings beyond financial assets alone.

- Diversification: Gold may respond differently than stocks and bonds in some market environments.

- Physical asset exposure: The account holds bullion, not just shares of a fund or mining company.

- Long-term hedge role: Some investors use precious metals as one layer of protection against inflation concerns, currency anxiety, or financial-system stress.

Those are possible uses, not promises. Gold can help with diversification, but it also has long stretches of weak or flat performance.

The costs are not just fees

Most articles stop at annual charges. The harder question is whether the structure delivers enough benefit to offset those charges and the added rules.

Two cost areas deserve close attention:

- Ongoing account expenses: setup, custodial administration, storage, insurance, and transaction spreads

- Behavioral cost: investors sometimes overallocate to gold because the metal feels safer than it is

- Compliance cost: one bad decision about storage or possession can create a tax problem far larger than the annual fees

That last point is the one investors miss.

The home storage trap can turn a retirement account into a taxable event

A common sales pitch suggests an IRA-owned LLC or "checkbook control" lets the account owner keep IRA metals at home, in a personal safe, or in a safe deposit box they control. That sounds efficient. It can also be the most expensive mistake in the whole setup.

The IRS explains in Publication 590-A and Publication 590-B that IRA assets are subject to specific custody and distribution rules. Tax professionals often warn that personal possession of IRA-owned precious metals can be treated as a distribution if the arrangement fails IRA requirements. If that happens, the metal's value may become taxable for that year, and an early-distribution penalty may apply for account holders under the applicable age threshold.

A simple way to read this is: if the retirement asset ends up under your direct personal control, the tax shelter may no longer hold up.

An IRA-owned LLC does not automatically fix that problem. The LLC is just a legal wrapper. It is not a free pass to ignore custody rules. Investors who hear phrases like "home storage IRA" or "store your IRA gold yourself" should slow down and get a written opinion from a qualified CPA or tax attorney before signing anything.

Storage choice affects both cost and peace of mind

Storage is not just an administrative detail. It is one of the main tradeoffs in a Gold IRA.

Commingled storage usually costs less. Your metals are held with metals of the same type owned by other clients, while records track your account's holdings. For many investors, that is enough.

Segregated storage usually costs more. Specific coins or bars are stored separately for your account. Investors who care about exact item identification, or who are holding larger balances, may prefer it.

A practical way to compare the two is to ask two questions:

- Do I care about receiving the exact same bars or coins back later?

- Is the added annual cost small enough relative to my account size and holding period?

For a modest account, segregated storage can eat up a noticeable share of the expected benefit. For a larger account, the extra cost may be reasonable if it improves clarity and comfort. The best choice is not the fanciest option. It is the option whose cost matches the size and purpose of the allocation.

How to reduce the biggest risks

Investors usually lower their odds of trouble by keeping the process boring and well documented.

- Get storage terms in writing. Verbal promises about home possession or special exceptions are not enough.

- Use only clearly eligible metals. "Rare" or promotional coins often create confusion.

- Read the fee schedule line by line. Ask about setup charges, annual administration, storage, insurance, and selling spreads.

- Question any loophole-based pitch. If the sales message focuses on getting around custody rules, assume the risk is higher.

- Keep the allocation proportionate. Gold can play a role in retirement savings without becoming the whole strategy.

The best risk control is simple. Treat a self directed Gold IRA as a specialized retirement account, not as a workaround for personal possession. That mindset helps separate legitimate diversification from expensive compliance mistakes.

Your Gold IRA Checklist and Next Steps

A lot of the confusion around Gold IRAs comes from trying to solve everything at once. A shorter checklist makes the decision easier because it separates suitability, compliance, and logistics.

A practical due-diligence checklist

Before opening a self directed Gold IRA, an investor should work through the basics:

- Clarify the role in the portfolio: Is this meant for diversification, inflation concern, or long-term tangible exposure?

- Assess time horizon carefully: Because of setup and storage costs, this structure is usually better suited to longer holding periods than quick tactical moves.

- Review the rollover path: Existing retirement funds need a clean, documented path into the new account.

- Confirm eligible metals before buying: Product mistakes can create avoidable compliance problems.

- Understand the storage choice: Commingled and segregated storage solve different concerns.

- Read the fee schedule line by line: Setup, administration, and storage should all be clear before funding.

- Ask who does what: The custodian and depository have different roles.

- Avoid any “store it yourself” pitch: That's where many of the worst tax surprises begin.

What a thoughtful next step looks like

A smart next step usually isn't rushing into a purchase. It's gathering the account documents, rollover details, and storage options in one place, then reviewing them with a qualified professional who understands retirement-account rules.

The strongest Gold IRA decisions usually come from slow, boring due diligence. That's a good thing.

This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions. Rules can change, and the right account structure depends on individual circumstances.

Frequently Asked Questions About Gold IRAs

Can someone put gold they already own into a Gold IRA?

Usually, investors should think of the IRA as buying its own assets through the proper account process. Personally owned metals and IRA-owned metals are not the same thing. Mixing the two can create compliance issues.

Can an investor store IRA gold at home?

No. As covered earlier, IRS rules require approved third-party possession for IRA metals, and personal possession can turn the holding into a taxable distribution.

How do distributions work in retirement?

Distributions can generally happen in cash or in kind, depending on the account arrangement and the investor's circumstances. In a cash distribution, the metals are sold and the proceeds are distributed. In an in-kind distribution, the metals themselves are distributed out of the IRA. The tax result depends on account type and individual tax circumstances.

Is a Gold IRA different from a Silver IRA?

The account structure is basically the same. The difference is the underlying metal. Eligibility rules for silver use a different purity threshold than gold, which is why product selection still needs to be checked carefully.

Is a self directed Gold IRA appropriate for everyone near retirement?

No. It may fit investors who want tangible assets and are comfortable with added rules, fees, and administration. It may be less attractive for investors who want maximum simplicity, low costs, or income-producing retirement assets.

If a reader wants a neutral place to continue researching, Gold IRA Association offers educational guides, rollover resources, and company comparison content designed to help pre-retirees evaluate their options. A simple next step is to compare top Gold IRA companies or speak with a specialist at 888-910-8386 before making any account decision.