The Austrian Silver Philharmonic is eligible for a Silver IRA because it contains 1 troy ounce (31.103 grams) of.999 fine silver, which meets the IRS minimum purity requirement for silver held in a precious metals IRA. The part that trips up many U.S. investors isn't the coin itself. It's the process for buying it through the right custodian and storing it correctly inside the account.

A lot of retirees reach this question after looking for a familiar silver coin that feels more established than a generic round but less expensive than some domestic bullion options. The Austrian Philharmonic often shows up on that short list. It has a long-running mint program, strong recognition, and a reputation for being a practical bullion coin rather than a novelty item.

Still, "IRA eligible" doesn't mean "buy it anywhere and put it in retirement savings however you want." U.S. rules add a layer of procedure. The coin's European origin, euro face value, and handling through a self-directed IRA all matter in ways most basic coin guides never explain.

Your Complete Guide to the Austrian Philharmonic Silver Coin

For a U.S. retiree exploring silver for portfolio diversification, the Austrian Philharmonic can make sense. It is a sovereign-minted bullion coin, it meets the purity standard required for silver IRAs, and it has broad global recognition. Those are the easy parts.

The harder part is understanding how this coin fits inside an American retirement account. A person can't buy Philharmonics personally and then drop them into an IRA later. The purchase, custody, and storage all have to follow IRA rules from the start.

Why this coin gets attention

The Austrian Philharmonic silver coin appeals to retirement investors for a few practical reasons:

- Recognizable bullion format: It is a standard 1 ounce sovereign coin rather than an odd-sized specialty product.

- IRA-compatible purity: Its .999 fine silver content puts it in the investment-grade category used for precious metals IRAs.

- European denomination: Its €1.50 face value gives it a distinct identity among major bullion coins.

- Lower entry cost at purchase: In many market conditions, it carries a lower premium than some better-known U.S. alternatives.

That last point catches attention fast, especially for investors who care more about total ounces acquired than about collecting prestige.

Practical rule: A coin can be perfectly acceptable for an IRA and still become a problem if the investor uses the wrong buying path, the wrong custodian, or personal possession.

What matters most for retirees

The main decision isn't just whether the coin is "good." It's whether the investor values:

- lower purchase premiums,

- global brand recognition,

- smooth IRA administration,

- and likely resale convenience in the U.S. market.

For many readers, that means weighing the Austrian Philharmonic silver coin as a retirement asset, not as a collector's item. That distinction matters because retirement planning usually rewards simplicity, compliance, and liquidity over novelty.

The History and Design of a Bullion Classic

Before money goes into any physical asset, background matters. A coin with a long production history and stable design usually feels easier to evaluate than one tied to changing themes or limited releases.

The Austrian Silver Philharmonic has that kind of continuity. According to Provident Metals' history of Austrian silver bullion coins, the Austrian Silver Philharmonic was first minted in 2008, while the broader Vienna Philharmonic series began in 1989 as a gold coin. The silver version debuted with a nominal face value of 1.5 euros.

A coin tied to Austria's musical identity

This coin doesn't borrow its identity from a national animal or a patriotic emblem. Its theme is music. That gives it a very different feel from many bullion products.

The design honors the Vienna Philharmonic Orchestra and Austria's musical heritage. Investors often appreciate that the imagery has remained stable because consistency makes a bullion coin easier to recognize at a glance.

What appears on the coin

The Austrian Mint, also known as Münze Österreich, produces the coin as Austria's official silver bullion coin. The imagery is well known among bullion buyers:

- Obverse side: the Great Organ of the Golden Hall in Vienna

- Reverse side: a group of orchestral instruments, including a cello, violins, a bassoon, a harp, and a Viennese horn

That artistic theme does more than make the coin attractive. It gives the coin a recognizable identity that has helped it become a staple in European bullion markets.

A retiree doesn't need to care about coin artistry to make a sound IRA decision, but a stable design from a government-backed mint does support recognition and confidence.

Why the history matters

When a coin has been minted every year since its silver debut, buyers and dealers know what it is. That kind of familiarity can support liquidity and make pricing easier to understand.

For retirement investors, the key takeaway isn't romance or tradition. It's credibility. A sovereign-minted coin with a long-running program is easier to evaluate than a niche product that may confuse future buyers.

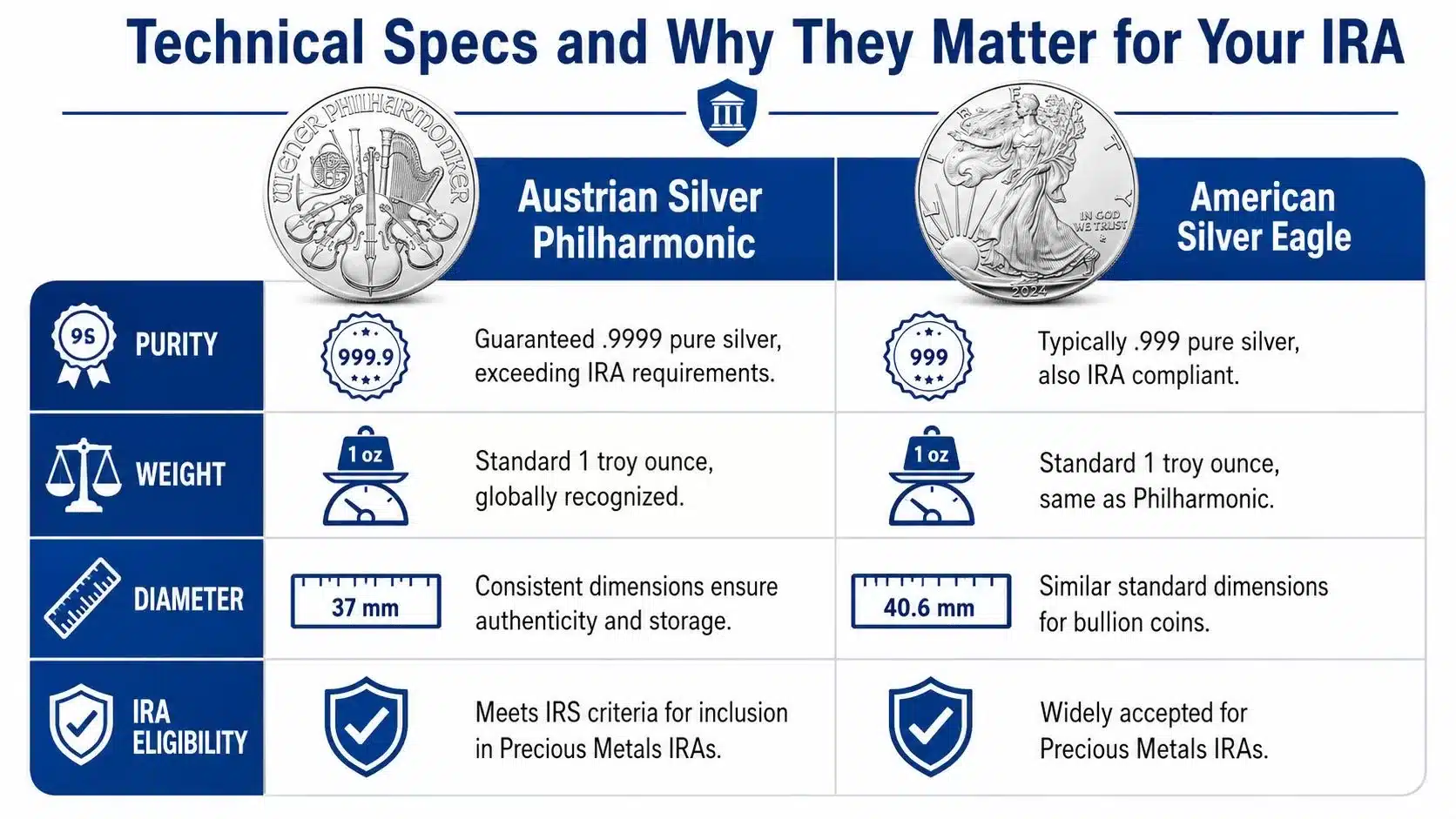

Technical Specs and Why They Matter for Your IRA

The Austrian Philharmonic's technical details are where the IRA conversation becomes concrete. Bullion coins don't qualify for retirement accounts because they're famous or attractive. They qualify because they meet the required standards.

According to SD Bullion's Austrian Philharmonic silver coin guide, the coin is struck from .999 fine silver, weighs exactly 1 troy ounce, and meets the IRS minimum purity requirement of 99.9% for silver IRA eligibility.

The specs that matter

Here are the core specifications that retirement investors usually care about most:

| Feature | Austrian Silver Philharmonic |

|---|---|

| Silver content | 1 troy ounce (31.103 grams) |

| Purity | .999 fine silver |

| Diameter | 37 mm |

| Thickness | 3.2 mm |

| Face value | 1.5 euros |

Only one line in that table drives IRA eligibility directly. It's the purity standard.

Why.999 fine silver is the key

For a self-directed precious metals IRA, the IRS requires silver to meet a minimum purity standard. This coin does. That's why it belongs in the same general conversation as other IRA-approved bullion products, while many collectible or lower-purity silver coins do not.

A lot of confusion comes from the word "collectible." Some coins look collectible because they're beautiful or internationally known. But for IRA purposes, what matters first is whether the product meets the bullion rules and is handled through the correct IRA structure.

Readers who want a broader overview of acceptable silver products can review this guide to IRA-approved silver.

What these measurements help you do

The coin's standardized size and weight also help with practical verification. Dealers, custodians, and depositories work with recognized formats. A coin with consistent specifications is easier to catalog, ship, store, and authenticate than an unusual product with inconsistent dimensions.

That matters because retirement investing isn't only about selecting an eligible item. It's also about avoiding administrative friction later.

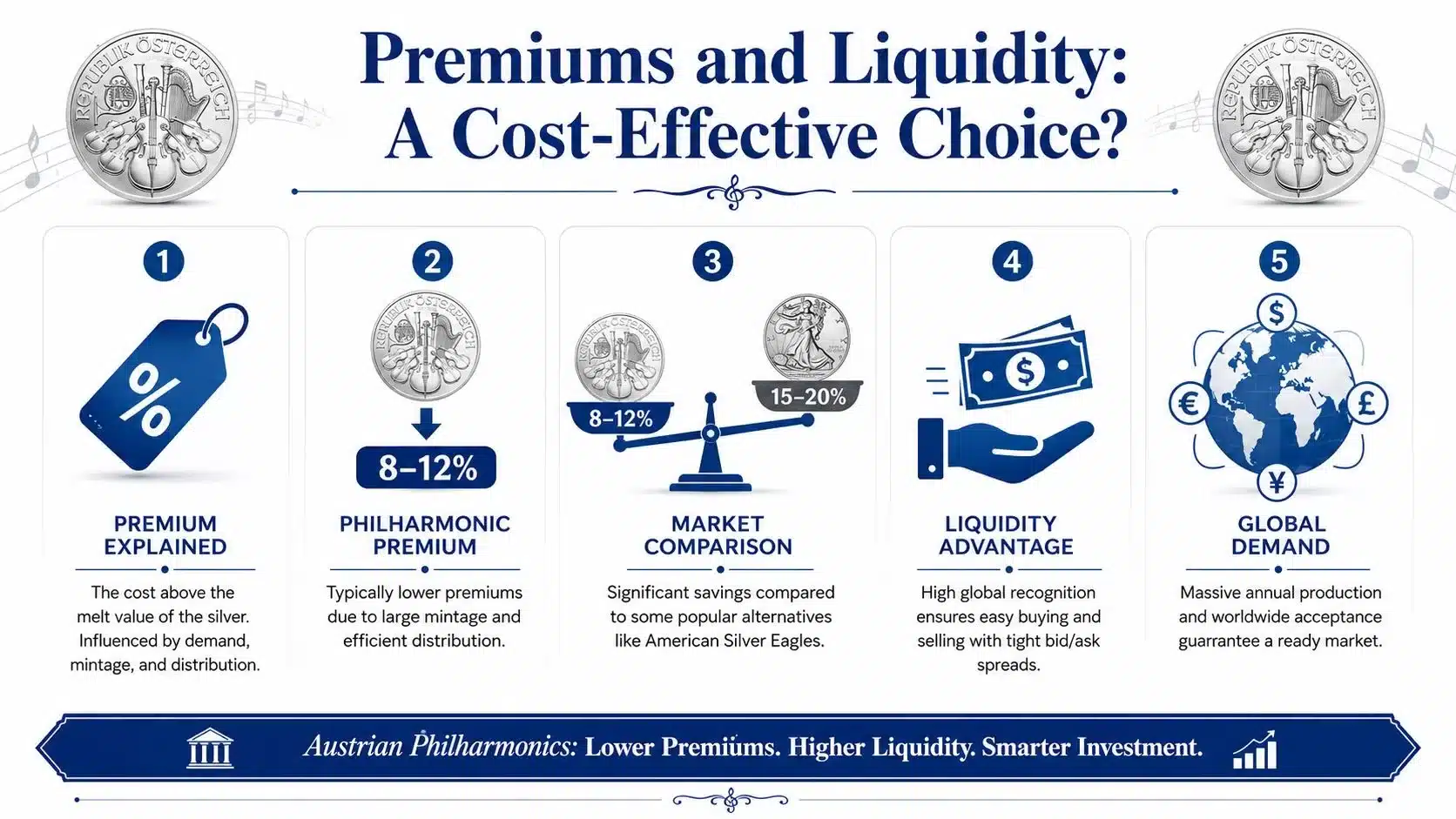

Premiums and Liquidity A Cost-Effective Choice?

Many buyers first notice the Austrian Philharmonic silver coin because it often costs less over spot than some better-known alternatives. That can be attractive for a retiree who wants to put more retirement dollars into silver content rather than into markup.

According to JM Bullion's Austrian Silver Philharmonic pricing overview, the Austrian Silver Philharmonic typically trades at about $6 to $7 over spot, while the American Silver Eagle often carries a premium of about $13 to $15 over spot.

Why lower premiums matter

A premium is the amount paid above the underlying silver value. In simple terms, it's the extra cost for minting, distribution, dealer margin, and market demand.

For a retirement investor, lower premiums can mean one important thing. More of the purchase goes toward actual silver exposure rather than toward overhead and brand pricing.

That doesn't automatically make the Philharmonic the better choice for every account. It does mean the buyer should ask a sharper question: is the additional premium on another coin likely to be recovered later?

The trade-off in the U.S. market

Many short articles stop too early. Lower purchase cost is only half the story. Resale conditions matter too.

The Philharmonic is globally recognized, but U.S. buyers sometimes place more emotional value on domestic bullion. That can affect secondary-market spreads, dealer preference, or how quickly a coin moves when the owner decides to sell. The coin may still be liquid. It just may not command the same enthusiasm from every buyer in every local market.

Lower premium at the time of purchase doesn't always mean better net outcome at the time of sale. The spread matters as much as the sticker price.

A practical way to evaluate the choice

A retiree comparing silver coins inside an IRA can think in three filters:

- Cost to enter: How much over spot does the coin usually cost?

- Ease of resale: Will common buyers and dealers in the investor's market recognize it quickly?

- Portfolio role: Is the goal lowest cost silver exposure, or a coin with stronger U.S.-centric brand pull?

Investors who are still comparing options at the account level can review best Silver IRA companies before deciding how the purchase will be executed.

How to Hold Philharmonics in a US Silver IRA

Knowing the Austrian Philharmonic qualifies is useful. Knowing how to hold it correctly is what protects the account.

According to Provident Metals' Philharmonic FAQ for collectors and IRA buyers, U.S. retirees must address custodial hurdles and storage nuances when holding Euro-denominated coins in U.S. depositories, because IRA-held metals are managed by a trustee rather than by the investor personally.

A clear process helps remove most of the confusion.

The basic chain of custody

In a compliant setup, the investor doesn't personally buy the coins and store them at home. Instead, the account uses a custodian and approved storage.

The process usually works like this:

Open a self-directed IRA.

The account has to permit physical precious metals.Fund the account.

Many retirees do this through a transfer or rollover from an existing retirement account.Choose the metal through the IRA structure.

The investor selects an eligible silver product such as the Austrian Philharmonic.The custodian executes the purchase.

Funds move from the IRA, not from the investor's personal checking account.The coins go to an approved depository.

They are stored in third-party custody, not in the investor's home safe.

That final point is one of the biggest areas of misunderstanding.

What investors can't do

A retiree can't keep IRA-owned coins in personal possession and still expect the account to retain its tax-advantaged treatment. That's a line many newcomers don't realize exists until they're already shopping for metals.

This overview of precious metal IRA rules helps clarify the broader framework.

A short video can make the process easier to visualize before speaking with a custodian or specialist.

Why the euro denomination doesn't change the process

The coin's €1.50 face value gives it a distinct identity, but it doesn't create a special exception for storage or custody. From a U.S. IRA perspective, the important issues remain eligibility, trustee control, and approved storage.

That means a retiree should focus less on the foreign denomination and more on these practical questions:

- Does the custodian support physical silver in the account?

- Will the dealer supply IRA-eligible Austrian Philharmonics?

- Which depository will receive and store the coins?

- How are purchase confirmations and holdings documented?

If those pieces are handled correctly, the coin can fit into a U.S. silver IRA in a straightforward way.

Tips for Authenticity and Safe Buying

Even a fully IRA-eligible coin can become a headache if it's counterfeit, mishandled, or sourced through a weak dealer network. That applies to retirement investors and personal buyers alike.

The first safety principle is simple. Buy recognized bullion through established channels. In an IRA, the investor usually works through a custodian and dealer arrangement, which adds a layer of process. Even so, the investor should still ask what exactly is being purchased and how it will be verified.

Practical checks that matter

Austrian Philharmonics are known bullion coins with fixed dimensions and weight. That consistency is useful. It gives buyers and storage providers a baseline for review.

Helpful checks include:

- Weight check: The coin should match the expected one-ounce bullion format.

- Dimension check: Standardized size helps identify obvious mismatches.

- Magnet test: Silver isn't magnetic, so a strong magnetic reaction is a warning sign.

- Sound or ping test: Experienced buyers sometimes use ring characteristics as an informal check.

None of these replaces professional verification. They help investors understand why recognized bullion products are easier to screen than obscure items.

A reputable seller matters more than any single home test. Most investors don't lose money because they skipped a magnet. They lose money because they trusted the wrong source.

Why IRA buyers still need this knowledge

Even when a retirement account handles the purchase, basic product knowledge helps the investor ask better questions. It becomes easier to confirm that the account is buying the intended sovereign bullion coin, not a lookalike product with similar branding or a non-eligible item.

Frequently Asked Questions

Is the Austrian Philharmonic silver coin IRA eligible?

Yes. The Silver Vienna Philharmonics product reference states that the 1 oz Austrian Silver Philharmonic contains one troy ounce (31.103 grams) of .999 fine silver, meets the IRS minimum purity requirement of .999 for inclusion in a precious metals IRA, and is produced by the Austrian Mint, a recognized sovereign mint.

Is it a collectible coin or a bullion coin?

For most retirement investors, it should be thought of as a bullion coin. Confusion happens because it has artistic design features and legal tender status, but the retirement decision usually centers on its bullion purity and IRA handling rather than on collector appeal.

Can someone buy the coin personally and place it into an IRA later?

Retirees should be cautious with that assumption. IRA metals generally need to be purchased and held through the proper IRA structure, with a custodian and approved storage arrangement. Personal possession creates risk.

Does the euro face value help or hurt U.S. investors?

It mainly makes the coin distinctive. The euro denomination doesn't remove U.S. IRA rules, and it doesn't by itself make the coin more useful inside a retirement account. The practical issues are still purity, custody, storage, and eventual liquidity.

Is the Austrian Philharmonic always the better choice than other silver coins?

Not always. It may appeal to investors who want lower premiums and international recognition. A different coin may appeal more to someone who prioritizes familiarity in the U.S. resale market. The better fit depends on the investor's goals, not on a universal ranking.

What's the most important takeaway before buying?

The Austrian Philharmonic silver coin can be a sound IRA option when the investor values recognized bullion and cost efficiency, but the purchase needs to be made through a compliant IRA process. Eligibility is only the starting point. Execution matters just as much.

If more help is needed sorting through custodians, eligible silver products, or rollover questions, Gold IRA Association offers educational guides and comparison resources for retirees who want a clearer next step. This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.