A lot of pre-retirees reach the same moment. They're looking at an old 401(k) or IRA, they're uneasy about market swings, and they want to know whether physical gold belongs in their retirement mix without creating a tax headache.

A good Gold IRA rollover guide should do more than list steps. It should help readers spot the decision points where costly mistakes happen, understand the rules in plain English, and move carefully if they decide a rollover makes sense. This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.

Are You Eligible for a Gold IRA Rollover?

A common frustration happens before any forms are signed. Someone has an old 401(k) or an active workplace plan, they decide they want part of it in physical gold, and then they learn the account may not be eligible to move yet.

That first checkpoint matters because eligibility depends on the retirement account rules, not on investment preference. If the account cannot be rolled over, the rest of the process stops there.

Accounts that may be eligible

Several account types can qualify, but each comes with its own rules:

- Old employer 401(k) plans: These are often the simplest place to start because the job has already ended.

- Traditional IRAs: These usually give the account owner more flexibility than an employer plan.

- Other employer-sponsored retirement plans: Some plans allow rollovers, but the plan documents control the answer.

- Roth retirement accounts: These can be eligible, but the tax treatment and rollover mechanics need closer review before any transfer begins.

A helpful way to look at it is this. Your retirement account is like money inside a container with its own lid and lock. Some lids open easily. Some only open under specific conditions. The mistake is assuming every container works the same way.

The early mistake that causes expensive delays

The most common problem at this stage is simple. People start paperwork before confirming whether their current employer's plan allows a rollover at all.

Current workplace plans often have tighter restrictions than old employer accounts. Some allow an in-service distribution, which means you may be able to move money while still employed. Others do not. If you skip that check, you can waste time, trigger confusion with custodians, or submit forms that the plan rejects.

Practical rule: If the money is still in a current employer plan, get the rollover rules in writing before doing anything else.

What to verify before you begin

Two documents usually give the clearest answer:

- The summary plan description

- The plan administrator's distribution or rollover rules

Ask direct questions and write down the answers:

- Does the plan allow rollovers while I am still employed?

- Is an in-service distribution available?

- Can I move only part of the balance, or does the plan limit partial rollovers?

- What forms or approvals are required before funds are released?

If the response is vague, pause. Ambiguity at this stage is often the first sign of a mistake that becomes expensive later.

Former employer plan vs. current employer plan

This distinction shapes the whole decision.

A former employer plan is often easier to roll over because your separation from service has already happened. A current employer plan may block distributions until you reach a certain age, leave the company, or meet another condition written into the plan.

That is why eligibility is less about market outlook and more about plan mechanics. A careful investor can choose the right metals, the right custodian, and the right timing, then still hit a wall if the plan itself does not permit the move.

If you want a broader explanation of what retirement accounts can hold and how the IRS treats them, review these precious metal IRA rules.

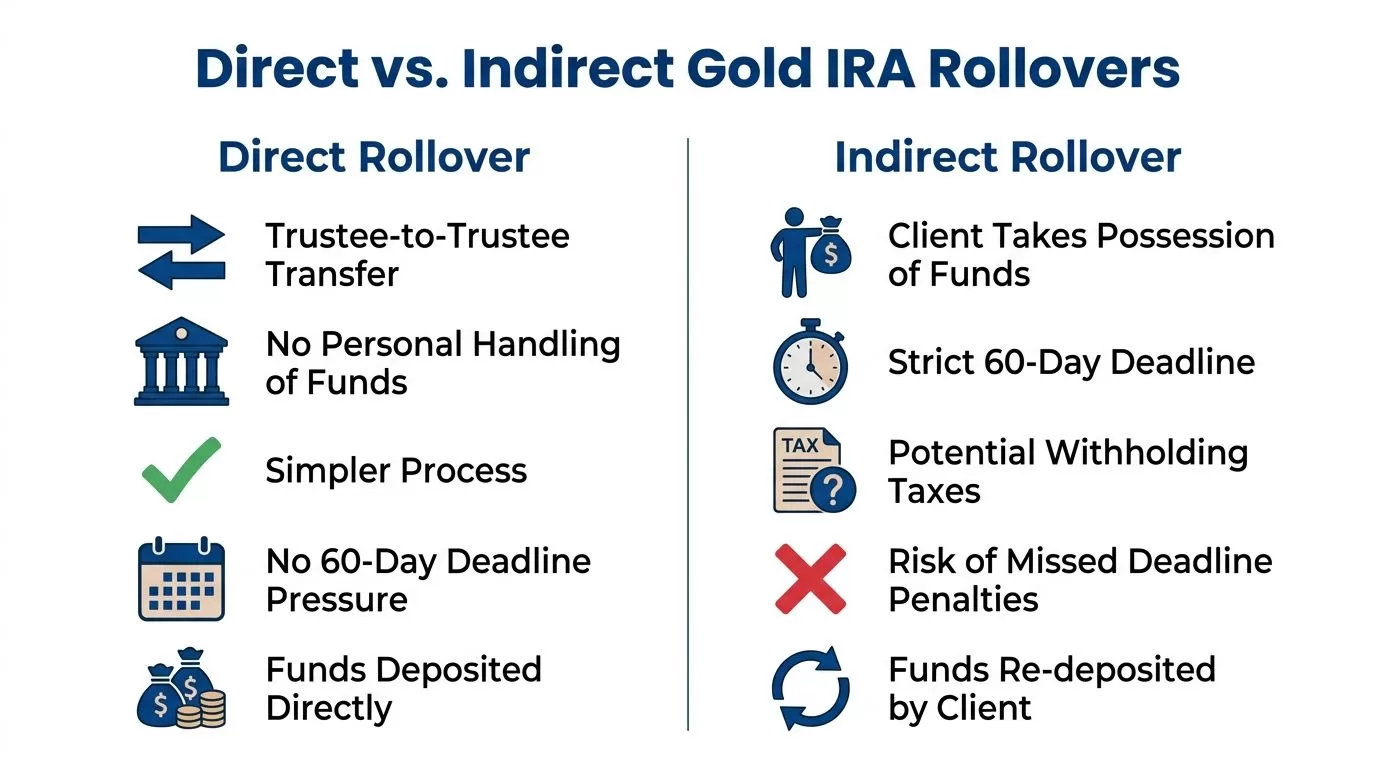

The Critical Choice Direct vs Indirect Rollovers

A common mistake happens right after approval. An investor gets the green light to move retirement funds, assumes both rollover methods are basically the same, and chooses the one that sends the money to them first. It feels straightforward. In practice, that choice creates more chances for a tax mistake, a missed deadline, or a shortfall that has to be covered out of pocket.

That is why this decision deserves more attention than a simple checklist usually gives it.

There are two main ways to move retirement money into a Gold IRA. A direct rollover sends the funds from one retirement institution to another. An indirect rollover sends the distribution to you first, and you then have to redeposit it into the new retirement account within the IRS time limit.

Why direct rollovers are usually the safer choice

A direct rollover usually causes fewer problems because the money does not pass through your personal bank account. The institutions handle the transfer, which reduces the odds of a paperwork error or timing issue.

A useful way to view it is this. A direct rollover works like handing a package from one courier to another with tracking attached. An indirect rollover puts the package in your hands, starts a countdown, and makes you responsible for getting it to the right destination in full.

That difference matters more than many investors expect.

The clearest risk in an indirect rollover

The withholding issue causes a lot of confusion. If your employer plan sends you the money first, part of the distribution may be withheld for taxes. To complete the rollover without creating a taxable event, you generally must redeposit the full distribution amount, not just the amount that landed in your account, and you must do it within the 60-day window.

Here is the part that catches people off guard. If money was withheld before you received the distribution, you may need to replace that missing amount from your own cash temporarily so the full rollover amount reaches the new IRA on time.

Many pre-retirees assume, reasonably, that redepositing the check they received is enough. It often is not. That misunderstanding is one of the costliest errors in the entire rollover process.

Direct vs. Indirect Rollover Comparison

| Feature | Direct Rollover (Recommended) | Indirect Rollover (Higher Risk) |

|---|---|---|

| Who handles the funds | Funds move directly between retirement institutions | You receive the distribution first |

| Deadline pressure | No 60-day redeposit rule for you to manage personally | You must meet the 60-day redeposit deadline |

| Withholding concern | Usually avoids mandatory withholding issues | Withholding can create a cash gap you must replace |

| Error risk | Lower administrative risk | Higher risk of timing and paperwork mistakes |

| Tax exposure if mishandled | Usually lower when set up correctly | Higher if the redeposit is late or incomplete |

A practical decision test

Ask yourself one question. Is there any good reason for me to personally handle these retirement funds if a direct institution-to-institution move is available?

For many investors, the answer is no.

A direct rollover is usually easier to document, easier to verify, and less likely to create an accidental tax bill. An indirect rollover can still be completed correctly, but it leaves less room for ordinary human error. If you are already comparing account types and transfer methods, this explanation of the benefits of a direct 401(k) rollover into a Roth IRA gives useful background on why direct movement is often preferred.

Where people get tripped up

The words rollover and transfer are often used casually, as if they mean the same thing. In retirement accounts, the mechanics matter. A lot.

The decision point is simple:

- Direct rollover: fewer moving parts, less hands-on risk, cleaner paper trail

- Indirect rollover: more responsibility on you, tighter deadlines, greater tax risk if anything is missed

An indirect rollover is not automatically wrong. It is the option that requires more care, more cash planning, and more attention to detail. For a Gold IRA investor trying to avoid preventable mistakes, direct is usually the cleaner path.

How to Choose a Reputable Gold IRA Company

A rollover involves more than selecting metals. It also requires choosing the firms that handle the account, the paperwork, and the storage arrangement. That's where due diligence matters.

The first thing to understand is that a custodian and a dealer are not the same thing. The custodian handles the IRA administration and compliance side. The dealer supplies the precious metals that the IRA purchases. Some readers blur those roles together, which makes it harder to compare what's being offered.

What good due diligence looks like

A reputable company should make the process clearer, not more confusing. If a provider leans on pressure, avoids direct answers, or can't explain the mechanics in plain English, that's a reason to slow down.

A careful review usually includes these checkpoints:

- Fee clarity: Ask for written detail on setup fees, annual account fees, storage charges, and any transaction-related costs.

- Role clarity: Confirm who the custodian is, who the metals dealer is, and where the metals will be stored.

- Education quality: Strong firms explain the rules before asking for a commitment.

- Service responsiveness: Good support matters because rollover paperwork often involves follow-up across multiple institutions.

- Reputation checks: Look for a consistent pattern of clear communication and issue resolution rather than polished marketing alone.

Questions worth asking before opening an account

Readers often get better answers when they ask narrow questions instead of broad ones.

- What does the full fee schedule look like in writing?

- Which institution serves as custodian?

- Which depository stores the metals?

- How is the rollover paperwork initiated and tracked?

- What happens if the current plan administrator delays the release of funds?

- How are buyback or liquidation requests handled later on?

A trustworthy provider doesn't rush the education step. It welcomes specific questions and answers them in writing.

Marketing appeal versus operational quality

Many companies sound similar at first. Most promise education, service, and retirement diversification. That's why readers should focus less on branding and more on operating details.

A strong company usually stands out by being organized. Documents are clear. Roles are defined. Fees are disclosed plainly. The conversation feels steady, not theatrical.

For readers who want to understand the administrative side in more depth, this overview of choosing an IRA custodian for gold is a useful next read.

Selecting IRS-Approved Gold and Silver

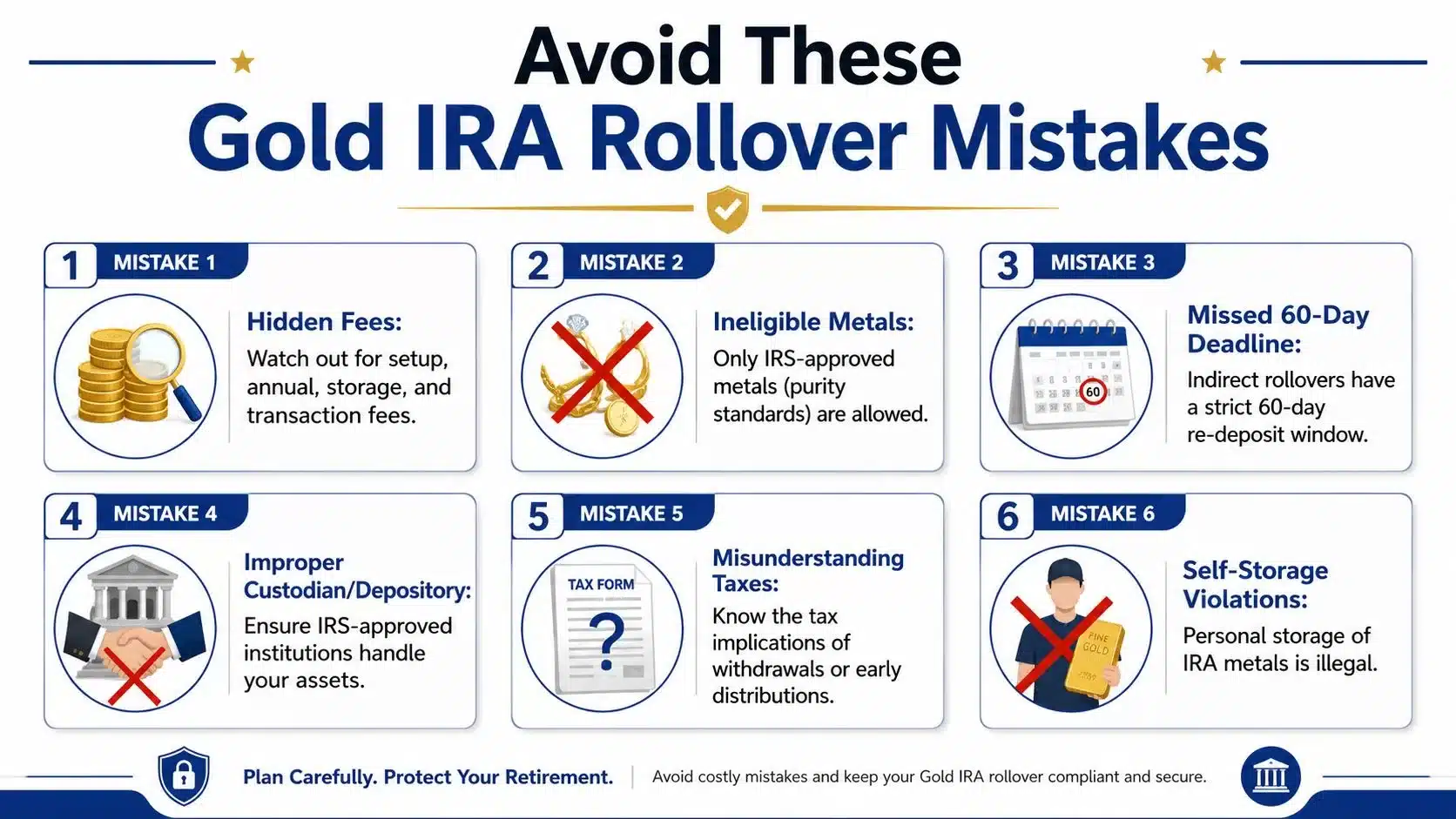

A common and expensive mistake happens after the rollover money arrives. An investor sees a gold coin that looks impressive, assumes any precious metal should work in a Gold IRA, and places an order before checking whether the item is allowed. That is how a simple purchase turns into a compliance problem.

The IRS does not approve metals based on appearance, brand appeal, or collector interest. It uses technical standards. For IRA purposes, gold bullion generally must be at least 0.995 pure, silver 0.999 pure, and platinum and palladium 0.9995 pure. Products outside those standards, along with many collectible items, do not qualify for IRA ownership.

What the purity rules actually mean

Purity is the first screen, not the only one.

A product can meet the metal threshold and still create confusion if it is marketed mainly for rarity or collector value. That is why experienced investors do not ask only, "Do I like this coin?" They ask, "Is this clearly eligible for an IRA, and can my custodian purchase and store it correctly?"

Gold IRA buying works more like stocking a regulated warehouse than building a personal collection. The account can hold certain forms of metal under specific rules, and the metal has to move through the right channels from purchase to storage.

The real decision point: bullion or collectibility

Many pre-retirees can take a costly wrong turn. Sales language around "exclusive" coins, limited editions, or historical appeal can make an item sound safer or more valuable than standard bullion. Inside an IRA, those features often add more confusion than value.

In plain English, the cleaner choice is usually standard bullion products with clear IRA eligibility. The more a product is sold for rarity, story, presentation, or numismatic appeal, the more carefully it should be reviewed.

A practical way to sort the options:

- Usually suitable: Standard bullion bars and coins that meet IRA purity rules and are commonly accepted by custodians

- Usually unsuitable: Jewelry, commemoratives, rare coins, and products sold mainly as collectibles

- Pause and verify: Any item where the seller cannot clearly document IRA eligibility before purchase

A safer purchase process

Before you approve a metal purchase inside the account, slow the decision down and confirm four points:

- Purity: Does the metal meet the IRS threshold for its category?

- IRA eligibility: Is the specific product approved for IRA ownership, not just precious metal in a general sense?

- Custodian execution: Is the purchase being made through the IRA structure rather than by you personally?

- Approved storage: Is the metal going directly to the depository tied to the account?

That short checklist helps prevent one of the most avoidable mistakes in the whole rollover process. Buying first and verifying later is backwards.

If the sales pitch centers on rarity, special packaging, or shipping the metals to your home, stop and confirm whether the product belongs in an IRA at all.

Keep the goal in view

A Gold IRA is a retirement account with narrow purchasing rules. It is not a side door for holding any coin or bar you happen to prefer.

The best decisions in this stage are usually the least complicated ones. Choose metals with clear eligibility, make sure the custodian handles the transaction properly, and avoid products that raise basic questions before the purchase is even made.

Avoiding Costly Mistakes Hidden Fees and Tax Traps

A common real-world mistake looks like this. An investor completes the rollover, feels relieved that the hard part is done, then learns months later that the account carries more ongoing costs than expected or that one casual decision created a tax problem.

That is why this stage deserves as much attention as the rollover paperwork itself. The expensive mistakes usually happen after the account is open, during routine decisions that seem small at the time.

Look at the full cost, not just the rollover

A Gold IRA can involve several layers of charges. The list often includes account setup, annual custodian administration, storage, insurance, and transaction-related costs tied to buying or selling metals.

The practical mistake is focusing on only one fee while ignoring the stack.

A useful way to evaluate the account is to ask for a written fee schedule and read it like a homeowner reads the full monthly housing cost, not just the mortgage payment. The headline number never tells the whole story. What matters is the all-in cost of keeping the account open year after year.

If a company explains fees vaguely, changes the subject, or focuses only on metal prices, slow down. Clear pricing is part of a good decision.

The tax trap that surprises investors

The most serious mistake is treating IRA metals like personally owned metals.

Inside a Gold IRA, the metals must stay under the account's custody and approved storage arrangement. If an investor takes personal possession or directs the assets outside that structure, the IRS can treat the account as distributed. That can turn a retirement move into a taxable event, and penalties may apply depending on age and circumstances.

The confusion is understandable. Buying gold for personal ownership is one thing. Holding gold inside a retirement account follows a different rulebook.

A simple way to remember it is this. Personal gold belongs under your control. IRA gold belongs under IRA control.

A short explainer can help reinforce the point:

Small mistakes that become expensive

Some errors do not look dramatic in the moment. They still cost money.

- Incomplete fee review: Ask for every account, storage, insurance, and transaction charge in writing before funds move.

- Casual custody decisions: Never assume IRA metals can be shipped to you, stored at home, or mixed with personal holdings.

- Poor recordkeeping: Save account forms, transfer instructions, trade confirmations, invoices, and storage documentation.

- Rushed approvals: Sales pressure is a signal to pause. Retirement accounts work best when each step is documented and understood.

- Selling without planning: Ask how liquidation works, what fees may apply, and how long the process usually takes before you need the money.

One final decision point matters here. If a choice feels slightly unclear now, it can become very clear after a bill arrives or a tax form is issued.

Bottom line: The costliest Gold IRA mistakes usually come from unclear fees, weak paperwork, and misunderstandings about custody. A careful review before you sign is much easier than fixing a tax problem after the fact.

Your Gold IRA Rollover FAQ

How long does a Gold IRA rollover usually take?

Timelines vary because multiple parties may be involved, including the current plan administrator, the new custodian, and the metals side of the transaction. Some moves are fairly smooth. Others slow down because paperwork sits in a queue or requires follow-up.

The practical lesson is to start before the money is urgently needed. A rollover is an administrative process, not a same-day trade.

Can IRA-owned gold be stored at home or in a safe deposit box?

No. IRA-owned precious metals must stay within the approved custody and depository structure described earlier in this Gold IRA rollover guide.

This is one of the clearest lines in the rules. Once investors treat IRA metals like personal metals, they risk turning the account into a taxable problem.

What happens when required distributions start?

Required distributions depend on the type of IRA and the investor's own tax situation. The key planning point is that physical metals can complicate distribution logistics compared with paper assets, because the account holder may need to sell metals or take an in-kind distribution if allowed under the account structure and tax rules.

Effective coordination is essential. Readers should review distribution planning with a qualified tax professional well before distribution requirements apply.

Can someone roll over a Roth 401(k) into a Gold IRA?

Possibly, but the structure needs to be handled carefully so the tax character of the money is preserved correctly. Roth money and pre-tax money don't work the same way, and that's not an area for guesswork.

The safest approach is to confirm exactly how the current plan labels the funds, then have the receiving custodian explain how that money would be accepted and reported.

Do investors buy the gold first and deposit it into the IRA?

No. The retirement funds move into the IRA as cash first, and then the custodian arranges the purchase within the account structure. The earlier cited Yahoo Finance source also notes that the deposited asset must be cash, and investors can't personally hold the gold first or deposit a different asset than the one withdrawn from the prior account.

That detail matters because some readers picture moving existing personal bullion into an IRA. That isn't how a compliant rollover works.

Is a partial rollover possible?

In many situations, investors may choose to move only part of eligible retirement funds rather than the entire balance. Whether that option is available depends on the rules of the existing account and the way the rollover is processed.

This can be useful for readers who want diversification without fully changing the makeup of their retirement holdings. The plan administrator can confirm whether partial distributions are allowed.

What's the safest overall approach?

For most readers, the safest path is the one with the fewest chances for error. That usually means confirming eligibility first, choosing a direct rollover structure when available, using clearly IRA-eligible metals, and keeping the assets under approved custody the entire time.

It's not a complicated idea. It's a disciplined one.

Gold IRA Association offers educational resources for readers who want to take the next step carefully. To continue researching without pressure, readers can compare top Gold IRA companies at Gold IRA Association. Those who prefer to talk through their options can also speak with a Gold IRA specialist at 888-910-8386.