A lot of readers asking how to buy gold in IRA are in the same position. They've built savings in a 401(k) or IRA, they're uneasy about market swings, and they want something tangible without tripping an IRS rule they didn't know existed. The process isn't hard, but the order matters.

The safest way to do this is simple. Choose the custodian first, fund the account second, select eligible metal third, and let the custodian execute the purchase and storage. That sequence prevents most expensive mistakes.

The First Step to Buying Gold in an IRA Is Choosing a Custodian

The biggest mistake new buyers make is shopping for coins before they've opened the right account. That's backwards.

A physical Gold IRA isn't a regular brokerage IRA. To hold bullion, the investor generally needs a self-directed IRA with a custodian that handles precious metals and the paperwork that comes with them. The custodian is the compliance gatekeeper. It receives instructions, processes the transaction, and makes sure the metal is held the right way.

What the custodian actually does

The custodian's role is practical, not cosmetic. It typically handles:

- Account setup so the IRA is structured to hold alternative assets like precious metals

- Transaction approval and recordkeeping when the account buys metal

- Coordination with storage providers so the gold goes to an approved depository, not to the account owner

- Reporting that keeps the account aligned with IRA rules

That's why the custodian choice is the most important decision in the whole process. A weak custodian creates confusion. A strong one prevents it.

Practical rule: If a company makes the metals sound exciting but stays vague about custody, storage, and paperwork, that's a bad sign.

How to compare custodians without getting sold

A cautious investor should use a checklist, not a sales pitch.

| What to check | Why it matters |

|---|---|

| Precious metals experience | Gold IRAs have unique compliance rules. General retirement account experience isn't enough. |

| Clear fee disclosure | If the fee explanation is fuzzy, the total cost usually won't improve later. |

| Responsive support | Gold IRA transactions involve forms, transfers, and approvals. Delays matter. |

| Operational independence | A custodian shouldn't box the investor into one dealer relationship without explanation. |

| Storage coordination | The process should be orderly and documented from purchase through delivery to storage. |

A good starting point is a dedicated guide to choosing an IRA custodian for gold.

The right mindset at this stage

This isn't the moment to chase a specific coin. It's the moment to build the legal container that will hold the investment correctly.

Readers who want to know how to buy Gold in IRA safely should treat the custodian like the foundation of a house. If the foundation is sloppy, every step after it gets riskier.

Funding Your Gold IRA with a Rollover or Contribution

Once the self-directed IRA is open, the next job is getting money into it. Most readers do that one of two ways. They either move existing retirement funds through a rollover or transfer, or they make a new annual contribution.

For the near-retiree audience, a rollover is usually the practical route. That's especially true for someone with an old workplace plan who wants part of those savings shifted into physical metals without taking a taxable withdrawal.

Direct rollover is the clean option

There are two ways people talk about moving retirement money. One is the direct rollover, where funds move from one retirement account custodian to another. The other is the indirect rollover, where the money passes through the account owner first.

A direct rollover is the safer path because it reduces the chance of accidental taxation, timing mistakes, and paperwork problems. If the goal is compliance and simplicity, that's the method to prefer.

Ask for a trustee-to-trustee movement of funds whenever possible. It keeps the money inside the retirement system and lowers the odds of a preventable error.

A common example looks like this:

- The investor opens a self-directed Gold IRA.

- The investor signs transfer or rollover paperwork.

- The current retirement plan sends funds to the new custodian.

- The cash lands in the new IRA.

- Only then does the investor choose metals for purchase.

That order matters because the IRA must be ready to receive the money before any buying decision happens. Readers who want a more detailed walkthrough can review this Gold IRA rollover guide.

Annual contributions still matter

Some investors won't roll over a large balance right away. They may start by contributing new money and learning the process with a smaller allocation.

For 2026, the annual contribution limit for a Gold IRA, treated as a traditional or Roth IRA, is $7,500 for individuals under age 50 and $8,600 for those age 50 or older, with the additional $1,100 representing the mandatory catch-up contribution for older investors, according to 2026 Gold IRA contribution rules.

A practical funding decision

The right question isn't “Can money go in?” It's “What's the least risky way to move it?”

Generally, that means:

- Use a direct rollover for old employer plans when eligible

- Use contributions if building the account gradually makes more sense

- Keep the paper trail for every transfer, contribution, and instruction

Investors often overfocus on the metal and underfocus on the movement of funds. That's a mistake. If the funding step goes wrong, the rest of the Gold IRA strategy gets much harder to fix.

How to Select IRS-Approved Gold Coins and Bars

Buyers often get burned by assuming any gold product can go into an IRA. It can't.

The IRS line is narrow, and the purity rule is the core filter. To legally hold physical gold in an Individual Retirement Account, the metal must meet a minimum purity of 99.5% fineness (0.995). The major exception is the American Gold Eagle coin, which is allowed at 91.67% fineness because of its legal tender status, as explained in this summary of IRA gold purity standards.

The fast filter to use before every purchase

Before approving any product, the investor should ask three questions:

- Does it meet the purity rule?

- Is it a recognized bullion product rather than a collectible item?

- Can the dealer and custodian confirm it is IRA-eligible before the order is placed?

If any answer is unclear, the product shouldn't go into the account.

Usually acceptable vs usually problematic

Simple lists are helpful here.

Common IRA-eligible directionally acceptable examples

- American Gold Eagle. The notable exception to the usual purity rule

- Gold bars meeting the required fineness

- Bullion coins specifically sold as IRA-eligible by approved channels

Common trouble spots

- Collectible coins marketed for rarity rather than bullion value

- Jewelry

- Random dealer inventory that hasn't been confirmed as IRA-eligible

- Coins a buyer already owns personally, because the IRA purchase must be executed through the proper account process rather than contributed in kind

A deeper reference list of IRA-approved gold coins can help confirm product categories before any order goes through.

Here's a quick visual explainer many readers find useful:

Why buyers get this wrong

The confusion usually comes from the word “gold.” Buyers hear “physical gold in an IRA” and assume purity, form, and classification are minor details. They aren't. Those details determine whether the asset qualifies or is treated as a prohibited collectible.

The right purchase isn't the coin that looks best in a brochure. It's the one the IRA is allowed to own.

That's why disciplined investors don't ask, “What gold do I like?” They ask, “What gold is eligible, documented, and easy to liquidate later?”

Executing Your Gold Purchase and Securing Storage

Buying gold inside an IRA doesn't work like buying a stock or ordering bullion for personal delivery. The account owner chooses the direction, but the custodian handles the compliant mechanics.

That distinction matters because the investor should never shortcut the process by trying to receive the metal first and sort out the paperwork later. That's how people create tax trouble.

What the purchase sequence usually looks like

Once the account is funded and the metal has been selected, the process is usually straightforward:

- The investor gives purchase instructions to the custodian

- The custodian sends funds from the IRA for the approved transaction

- The dealer fulfills the order

- The metals ship directly to the approved depository

- The custodian records the holding inside the IRA

The investor directs the process, but doesn't personally hold the funds or the gold during purchase and storage.

Storage is not optional

The storage rule is one of the strictest parts of a Gold IRA. The IRS requires physical gold in an IRA to be stored in a third-party, IRS-approved depository, and if the investor takes physical possession, the entire value is treated as a taxable distribution, according to this explanation of Gold IRA depository storage rules.

That means no home safe. No personal vault. No shipping the metals to the investor's address first.

A compliant Gold IRA is intentionally hands-off. The investor owns the asset through the IRA, but custody stays with approved institutions until a proper distribution happens.

What secure storage is supposed to accomplish

Approved depository storage serves a few practical purposes:

- Chain of custody so there's a documented path from dealer to depository

- Asset segregation and reporting inside the retirement account structure

- Protection of tax status by keeping the metals from becoming personal possession

The purchase step should feel uneventful. That's a good sign. Smooth, documented, and boring is exactly how retirement account compliance should work.

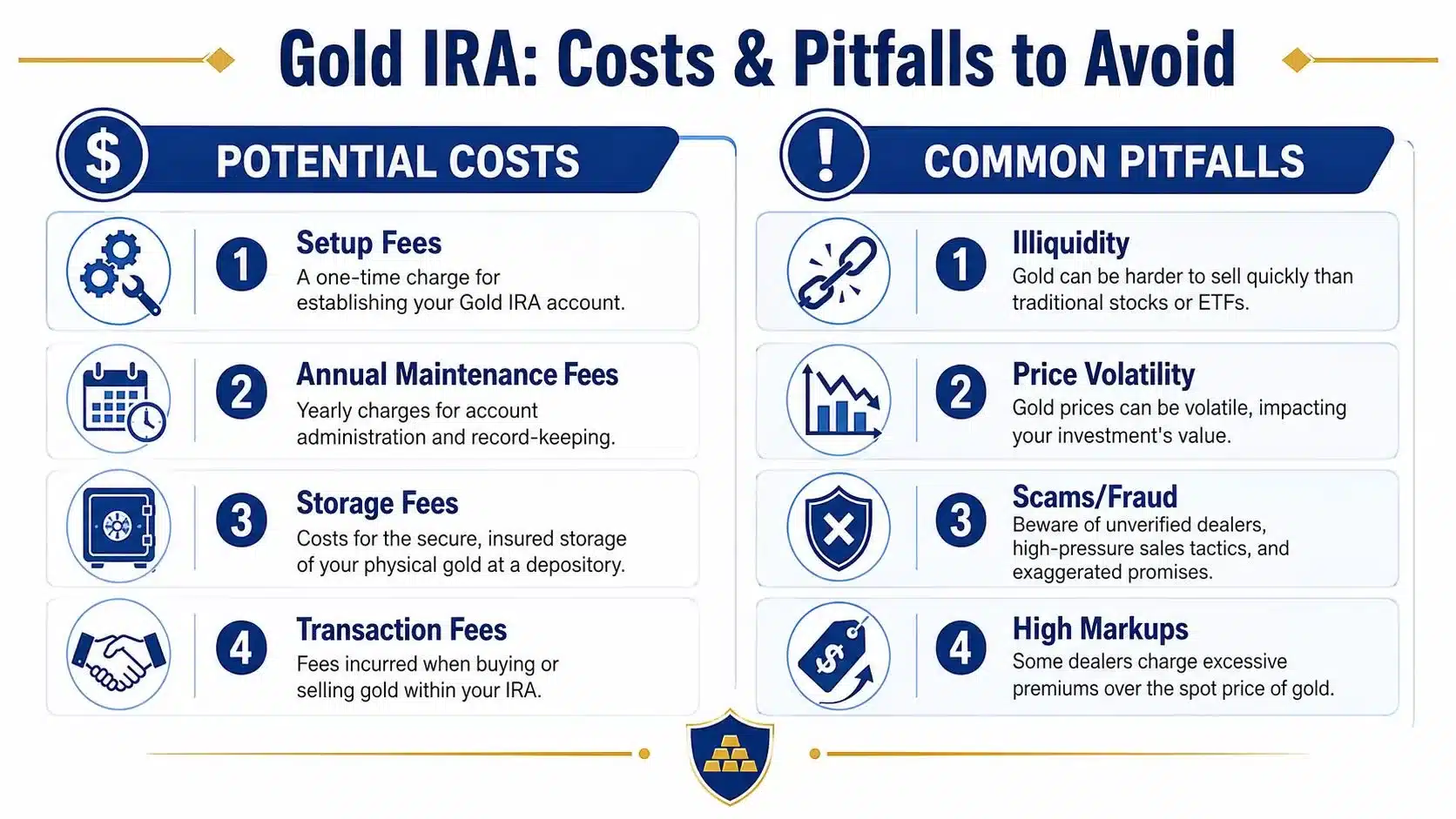

Understanding Gold IRA Costs and Common Pitfalls

Gold IRA marketing often makes the account sound simple on cost. It isn't. The visible fee is only part of the picture.

There are usually three layers to think about. Administrative account costs, storage costs, and transaction economics at the point of buying or selling. Investors who ignore the third bucket often misjudge what they're really paying.

The costs that deserve real attention

A realistic review should include:

- Setup charges tied to opening and establishing the account

- Ongoing custodian fees for administration and reporting

- Depository storage fees for holding physical metal

- Dealer spread or markup built into buy and sell pricing

None of those are automatically disqualifying. But they do mean a Gold IRA has to be evaluated as a full system, not just as “buying gold.”

Liquidity is weaker than many buyers expect

The hidden issue isn't only annual fees. It's liquidity.

Physically stored gold in a Gold IRA can require 3 to 7 days for sell-back and may involve bid-ask spreads of 3% to 5%, while ETFs can settle in seconds, according to this discussion of Gold IRA liquidity risk.

That matters most to retirees who may need access to cash quickly. Gold in an IRA can be useful for diversification, but it isn't the same as a button-click sale in a regular brokerage account.

A Gold IRA works best when the investor understands that convenience is lower and friction is higher than with paper gold products.

The mistakes that cost the most

Some pitfalls are operational. Others are behavioral.

| Pitfall | Why it hurts |

|---|---|

| Buying based on pressure | Urgency usually benefits the seller, not the retiree. |

| Ignoring spreads | A product can be “eligible” and still be expensive to enter or exit. |

| Confusing collectibles with IRA bullion | This can create a compliance problem before the account even gets going. |

| Overlooking sell-back process | Exit terms matter just as much as entry terms. |

| Treating gold as a cash substitute | Physical IRA metals are slower to liquidate. |

A blunt recommendation on costs

Investors should insist on plain answers before funding a Gold IRA:

- What recurring charges apply?

- How does the company handle liquidation?

- What kind of products are being emphasized, and why?

- Is the recommendation centered on bullion efficiency or on high-margin specialty items?

If those answers feel slippery, walk away. Gold can play a role in retirement planning. Overpriced gold inside a confusing IRA setup is a different thing entirely.

Answers to Common Questions About Gold IRAs

Even after the process is clear, a few questions usually linger. These are the ones that matter most because they sit right at the line between a compliant Gold IRA and an avoidable tax problem.

Can existing personal gold be added to an IRA

No. A Gold IRA must buy eligible metals through the IRA structure. Personally owned coins or bars shouldn't be dropped into the account after the fact.

That's one reason the sequence matters so much. The account comes first, then funding, then the IRA makes the purchase.

Can IRA gold be stored at home or in a safe deposit box

No. IRS rules prohibit storing IRA-held precious metals at home, in a personal safe, or in a private safe deposit box, and taking physical possession can trigger a taxable distribution of the entire account value, as outlined in this explanation of home storage restrictions for IRA precious metals.

That rule is strict enough that investors shouldn't test the edges of it.

How does someone take money out later

At retirement, there are generally two broad paths. The investor can liquidate metals inside the account and take cash distributions, or request distribution of the metals if eligible to do so under the account rules and tax treatment that applies at that time.

The exact tax effect depends on the individual's account type and circumstances. This is not financial advice. Consult a licensed financial advisor, CPA, or tax professional before making investment decisions.

What happens with required distributions in retirement

Once required minimum distributions apply, the account owner has to plan ahead. That may mean selling part of the metal position in time to meet the distribution requirement, or coordinating an in-kind distribution if appropriate.

The key issue is planning. Physical assets are less flexible than cash, so waiting until the last minute is a poor strategy.

Is a Gold IRA the same as buying gold personally

No. Personal gold ownership gives direct possession, but it doesn't carry the retirement-account structure. A Gold IRA gives tax-advantaged retirement account treatment, but in exchange the investor has to follow tighter purchase, custody, and storage rules.

That trade-off should be understood before any rollover starts.

Gold IRA Association publishes practical education for retirees and pre-retirees who want to understand Gold IRA rules before moving money. A sensible next step is to compare top Gold IRA companies or talk through the process with a specialist at 888-910-8386.